(Bloomberg) -- Intel Corp., revealing new details about its manufacturing operations, said that losses have deepened at the chipmaker's factory network and the business may not reach a break-even point for several years.

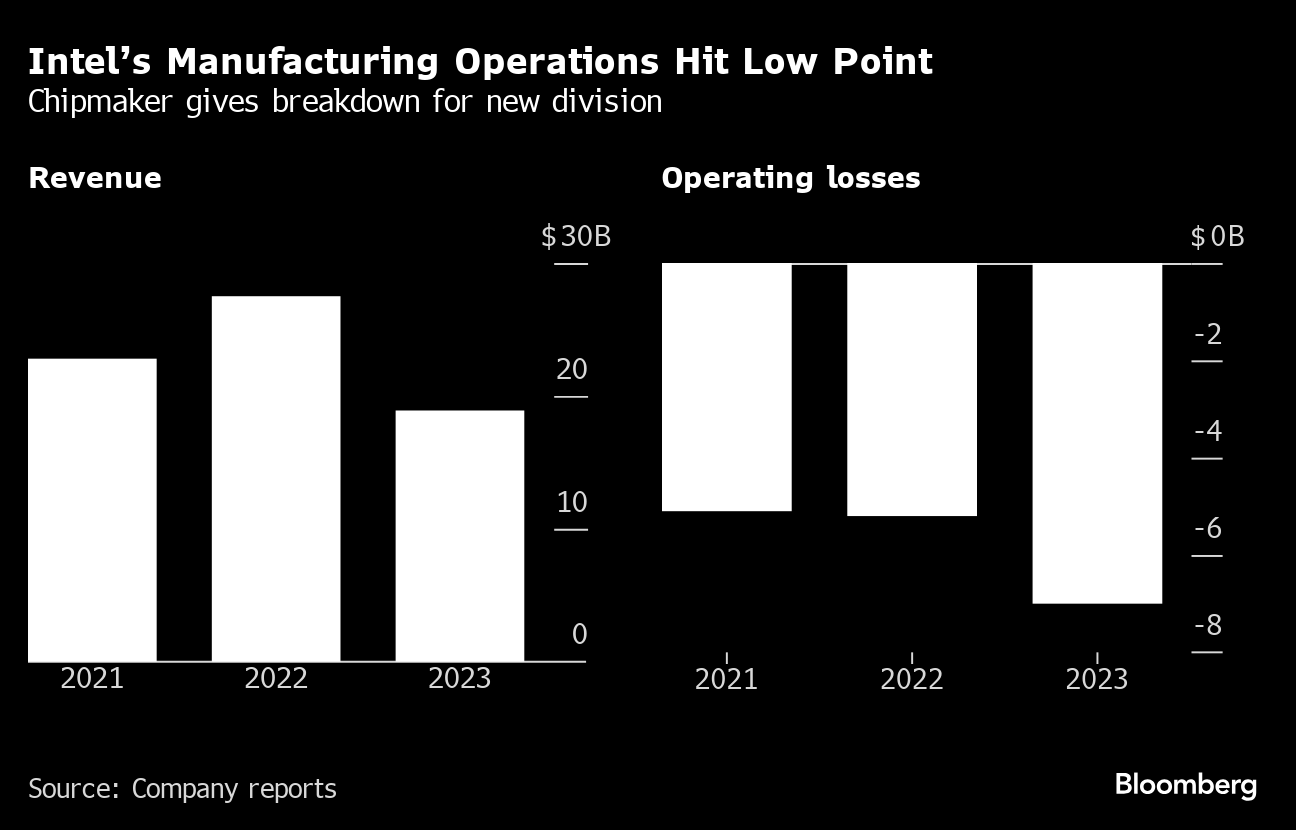

Intel Foundry, a new division of the company responsible for manufacturing, had sales of $18.9 billion in 2023, down from $27.5 billion the previous year, the company said late Tuesday. The operating loss at the new unit widened to $7 billion from $5.2 billion.

Intel fell more than 4% in extended trading after disclosing the numbers. The shares had been down 1.3% to $43.94 in regular trading Tuesday, bringing their year-to-date drop to 13%.

Intel is giving a more detailed picture of its finances as part of an ambitious turnaround plan by Chief Executive Officer Pat Gelsinger. He's breaking out the results from the factory network as a step toward having it operate more independently. The business is seeking to make chips for other companies, and giving it some separation from the rest of Intel is vital to that strategy.

The company's new timeline and financial targets show the challenges of the effort, which includes investing billions of dollars into new plants.

“We believe this transparency and accountability is needed,” he said during a presentation. “The required transformation is well underway.”

The company expects 2024 to be the peak of its losses and that Intel Foundry will be profitable, on an operating level, “midway between now and the end of 2030.” The chipmaker also named Lorenzo Flores as chief financial officer of the division.

Intel's push into outsourced chip production — known as the foundry industry — is one of the company's biggest transformations in its history. Gelsinger's comeback effort also includes restoring Intel's once-unassailable technology edge — something that the chip pioneer lost in the years before he took the reins in 2021.

Intel's struggles have forced it to outsource the manufacturing of some vital components, Gelsinger revealed in the presentation. It now buys about 30% of its silicon wafers, he said. But by improving Intel's technology — using a technique called extreme ultraviolet lithography — the company intends to bring more of this production back in-house, he said.

The CEO repeated his assertion that Intel will restore its technology advantage by next year. Over time, that will improve the capabilities of Intel's products and make them cheaper to manufacture. It will also allow the company to win orders from competitors, something that will provide as much as $15 billion in sales by the end of 2030, Gelsinger said.

Intel said there are five such companies committed to using its latest production technique, called 18A. It will become more widely used starting next year and gather momentum after that, the company said.

Taiwan Semiconductor Manufacturing Co. currently dominates the foundry market and has eclipsed Intel in overall revenue. That company had 2023 sales of $69.4 billion and net income of $26.9 billion. Its gross margin — the percentage of sales remaining after deducting the cost of production — was 54%. And its sales are projected to expand 20% in 2024 to $83.4 billion.

Intel's closest rival in its traditional business is Advanced Micro Devices Inc., which had revenue of $22.7 billion and net income of $854 million last year. Its gross margin was 50%. This year the company is on course for a sales jump of 14%, according to analysts.

Nvidia Corp., meanwhile, has quickly emerged as the star of the industry. Though it doesn't yet have the revenue of TSMC, its sales more than doubled last year — and another stratospheric gain is projected for this year. The company has a commanding lead in the market for artificial intelligence accelerators, which help companies develop AI models.

Intel has embarked on a record-setting expansion of its factories in the US and Europe, taking advantage of government incentives such as the Chips and Science Act. But even with that support, it's an expensive undertaking that has put investors on edge.

The company telegraphed earlier this year that its manufacturing finances are “under significant pressure” as the chipmaker tries to restore its technological capabilities and builds its infrastructure.

Chief Financial Officer Dave Zinsner, who joined Gelsinger in taking questions from analysts Tuesday, acknowledged that there's plenty of room for improvement. But separating out the manufacturing group — and treating the company's product division as a customer — has already yielded benefits, he said. There's been a huge reduction in expensive requests for expedited work and test chips, he said.

The company has also had some client wins. In February, Intel announced that Microsoft Corp.'s internal chip design effort will become a customer for the foundry business. Gelsinger has said he's ahead of schedule in getting other clients to sign up, but is unable to name them because they don't wish to go public.

(Updates with executive commentary in sixth paragraph.)

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.