It was nearly two years ago that the Reserve Bank of India clamped down on a small but fast-growing market for cryptocurrencies in the country. The regulator prohibited entities regulated by it from providing any services related to virtual currencies. That effectively killed the crypto market in India even though, technically, there is no legal ban on their use in the country.

Representatives of the crypto industry have challenged the diktat in the Supreme Court and a verdict is expected in the next few weeks.

In the meantime, India's crypto-community has changed tacks in the hope that eventually they will be able to come back to the Indian market in full force.

They are encouraged by estimates of the potential of the Indian market. According to Crebaco Global Inc., a credit rating and audit firm for blockchain and crypto companies, India has an immediate potential market size of $12.9 billion if the sector is regulated.

And so many of India's crypto entrepreneurs continue to adapt and keep their businesses alive in small ways.

From Exchange To Wallet

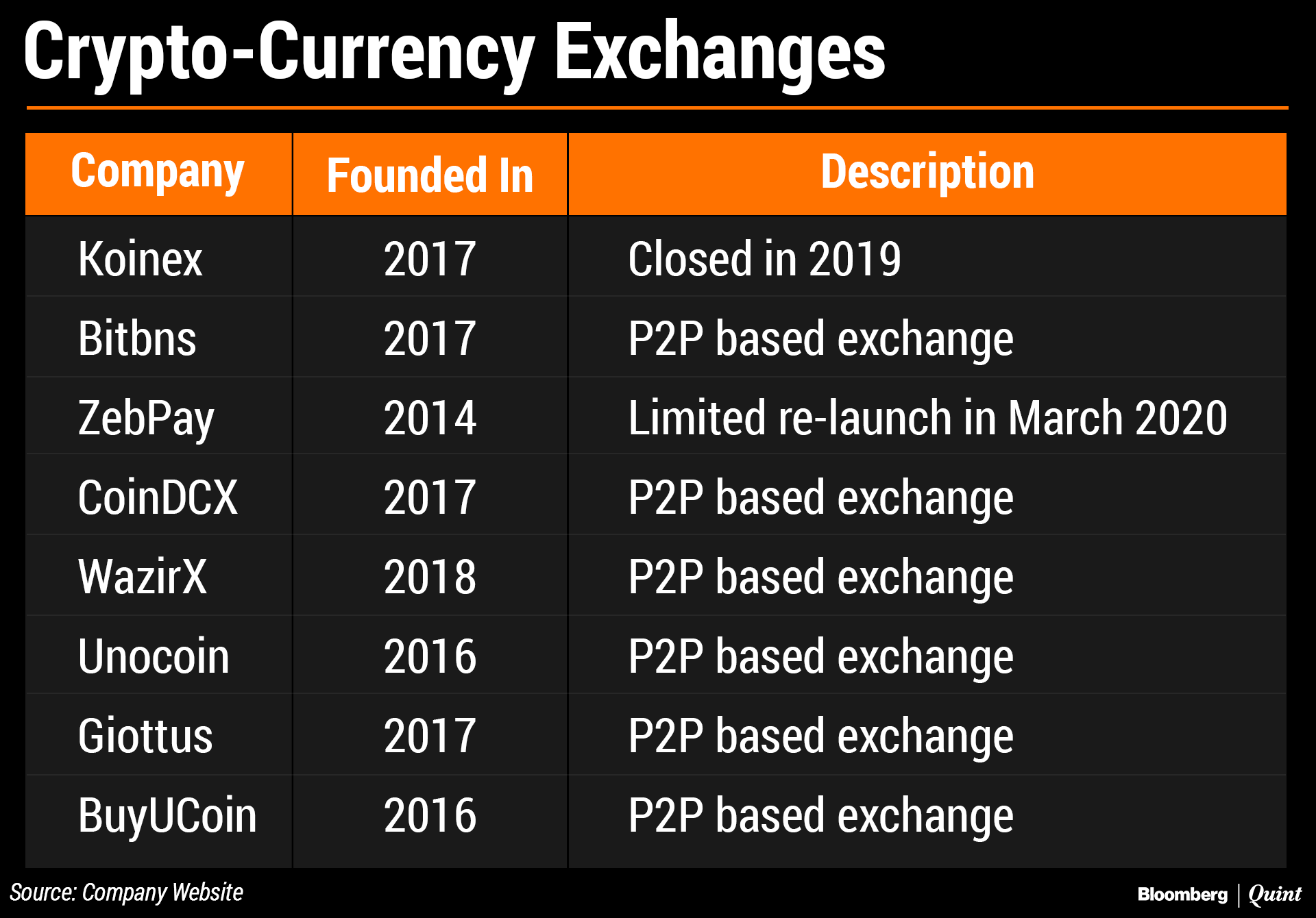

Zebpay was one of the leading exchanges in the country back in 2018. The lack of clarity on the legality of crypto currencies in India, however, hit the company hard.

“At the time of the circular, we held customer fiat money as well as crypto currency. We decided to return the fiat to customers until we could get the regulatory certainty we wanted. But we continue to hold crypto for the vast majority of those customers and we've been innovating in wallet security ever since," said Rahul Pagidipati, chief executive officer, Zebpay.

There are roughly 100,000 active users a month on the platform who can monitor their investments and pay for services in crypto but they cannot buy or sell, he said.

The company is planning to re-launch in March this year, with a crypto-to-crypto trading service across 150 countries, including India. “As regulations become clear, we'll expand our offerings. We don't want to jump the gun and hope to work with the government on converting fiat to crypto,” Pagidipati said.

Indian customers of international and domestic exchanges, that moved abroad in the past two years, continue to hold their crypto investments in a wallet. But they cannot cash out due to the RBI's restrictions.

They either have to arrange for cash through friends who are abroad or find local dealers on websites like LocalBitcoins or LocalCryptos, which help customers convert their crypto to cash.

Peer-To-Peer Crypto Trading

Other crypto firms have adopted a peer-to-peer model. Sort of a mini crypto system within India's broader financial system.

“We found that P2P is a better alternative for the Indian market. Users can buy cryptos in rupees or sell their cryptos for rupees. But instead of the money flowing through the exchange, the buyer and seller transfers the money between their banks,” explained Nischal Shetty, chief executive officer, Wazir X.

In November last year, Wazir X was acquired by Binance, one of the biggest crypto-currency exchanges in the world. Wazir X processes around $20-25 million worth of transactions a month, with 250,000 users, the majority of whom are Indians.

“In spite of no regulations, we mandate know-your-customer details and follow anti-money-laundering norms at the point of entry,” said Shetty, adding that crypto firms are ready to comply with any regulations that the government brings about.

Other P2P-based domestic-crypto exchanges include Giottus, Bitbns, BuyUCoin, UnoCoin and Coin DCX.

“The primary focus of this innovation (P2P-based transfers) was that the user would get the right value and the product would also respect and abide by the RBI decision,” said Sumit Gupta, CEO at Coin DCX.

According to a senior lawyer, who spoke on the condition of anonymity, while these companies are currently operating in a legal grey area, most of them are complying with existing norms on know-your-customer and anti-money laundering, indicating that the industry is open to regulation.

There are other companies that provide services to to crypto exchanges.

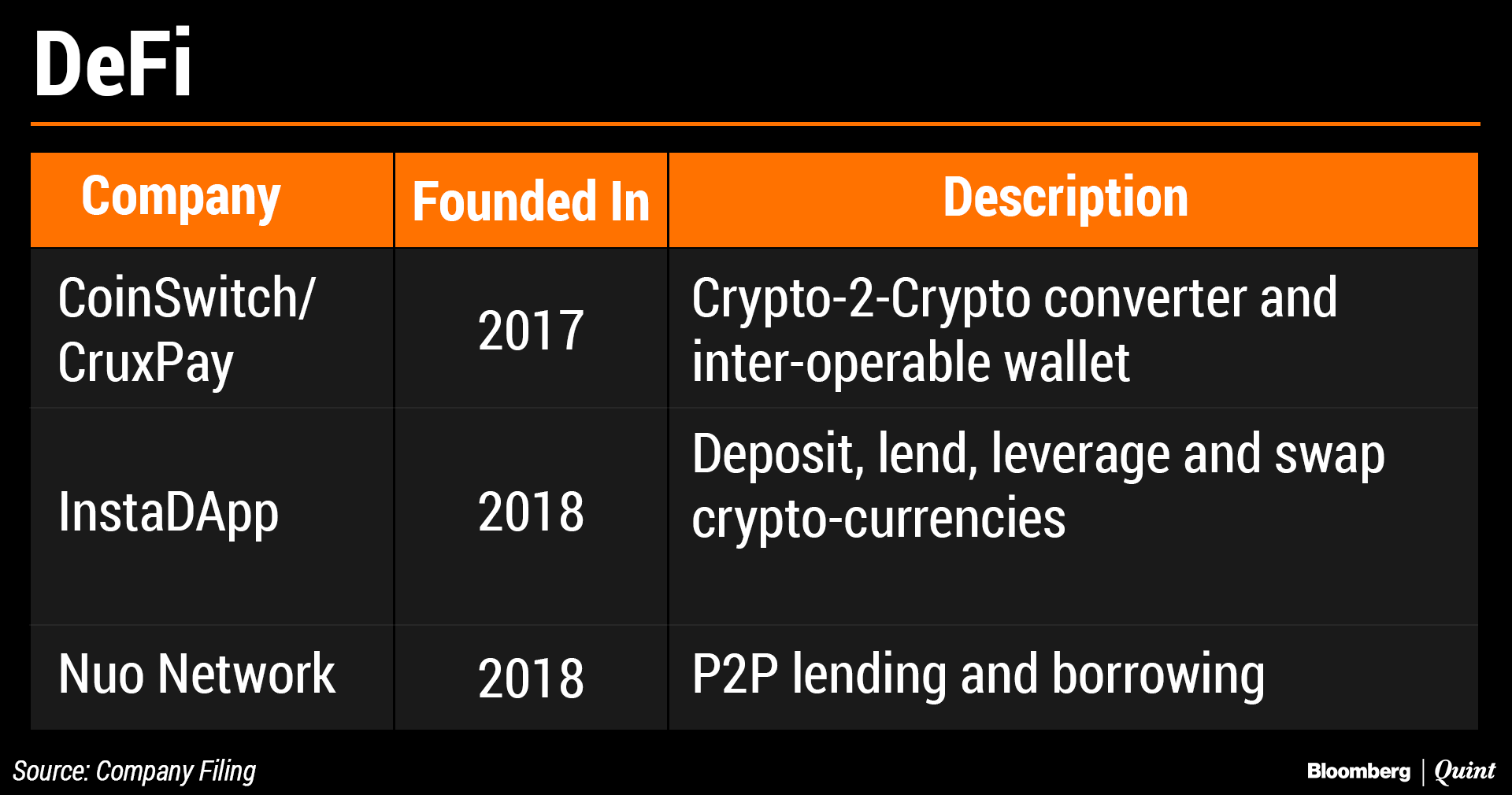

For example, Sequoia Capital-backed Coinswitch is an exchange aggregator, which lists the best prices for buying and selling cryptos across several global exchanges. The company also runs CruxPay, which is an interoperable wallet for crypto transfers. Through CruxPay, any crypto investor can make payments or transfers to another investor, regardless of which exchange they have bought it from.

Ashish Singhal, founder of both CruxPay and Coinswtich, told BloombergQuint that they operate across 160 countries and comply with regulations across these jurisdictions. In India, they have limited offerings and only list the prices of a limited number of cryptos across only a few global exchanges.

Decentralised Finance And Services

Another model catching the attention of entrepreneurs is decentralised finance or DeFI. This is essentially financial services built on blockchain networks where the instrument of finance is a cryptocurrency like Bitcoin or Ethereum.

While P2P trading has taken root in India, P2P lending on DeFi platforms has only recently begun with companies like Nuo Network and InstaDapp.

Souwmay Jain, founder, InstaDapp, said the platform provides P2P lending and borrowing services whereby a lender can park cryptos in a pool and earn interest on their holdings from borrowers. The interest comes in cryptocurrency as well. “The smart wallet developed by the company allows users to borrow, lend, leverage, swap cryptos,” Jain said.

The company is already making strides globally and is the third-largest custodian of cryptos for lending services, with $82.3 million worth of Ethereum locked on the platform, according to DeFi Pulse.

What Lies Ahead

Most immediately, India's crypto geeks are watching the Supreme Court verdict and hoping for relief.

But the battle may not end there.

Last year, a government panel headed by the Department of Economic Affairs proposed a penalty, as well as a jail term up to 10 years, for those mining, generating, holding, selling, transferring or issuing cryptocurrencies directly or indirectly.

A final decision on regulations governing cryptocurrencies is yet to be taken.

In the meantime, the tough regulatory stance has hurt India's standing in the global crypto markets, said Raj Chowdhury, managing director at HashCash Consultants. Companies that started here could have been global players and innovators by now; instead either they scaled down their operations or shutdown completely, Chowdhury said.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.