UBS has initiated coverage on Hindustan Aeronautics Ltd. with a 'buy' rating because it expects the company's order book to triple by fiscal 2026.

The aerospace and defence company has a $10 billion-plus order book, and it could benefit from the $60 billion of more defence aircraft orders from now till FY28E. Of this, $16 billion have already been approved and $40 billion-plus with higher local content should be awarded in the next 5-7 years, according to UBS Global Research.

"We expect the depletion of India's military aircraft strength in the coming few years, geopolitics and a need for greater aircraft availability to accelerate ordering and lead to a manufacturing ramp-up at HAL vs. the past decade," the research firm said in a Jan. 4 note.

HAL is set to triple its order book from Rs 0.8 trillion in FY23 to Rs 2.4 trillion in FY26E. "We believe HAL is on course to re-rate by a similar magnitude to Bharat Electronics in the past decade, if it gets its execution right," UBS said.

The brokerage has set a target price of Rs 3,600 apiece on the stock, implying an upside return of 23%.

New Orders To See Revenues Rising At 16% CAGR

HAL recently expanded its Tejas Mk1A fighter aircraft manufacturing capacity from 8 to 16 per year and is working to expand it further to 24—with two new lines at the Bengaluru complex and another at Nashik—sufficient to deliver 10 squadrons over FY23–32E, based on our platform-wise production assessment, UBS said.

It has also expanded its rotary wing platform's manufacturing capacity to meet growing demand for locally designed and manufactured aircraft.

"We believe consensus estimates have not yet built in faster order completions, HAL's ability to ramp up production and improve manufacturing value add, and a defence eco-system in India spanning government, SOEs, and Tier II and III defence companies that is becoming increasingly responsive," the brokerage said.

Own-Design Manufacturing To Drive Double Digit EPS

With the government seeking to reduce import dependence and promote domestic manufacturing in the defence sector, the past decade has seen a steady reduction in import components for HAL, from 85% in FY13 to 77% now.

Several HAL-designed aircraft platforms, such as the Tejas Mk1A, are gaining acceptance from the Indian military.

"We forecast 16%/18% top-line/net income CAGRs for HAL during FY23-26E with a 20% ROE, implying stable gross margin, despite an adverse revenue mix, as we expect higher local content and lower staff costs to support Ebitda margins," the brokerage said.

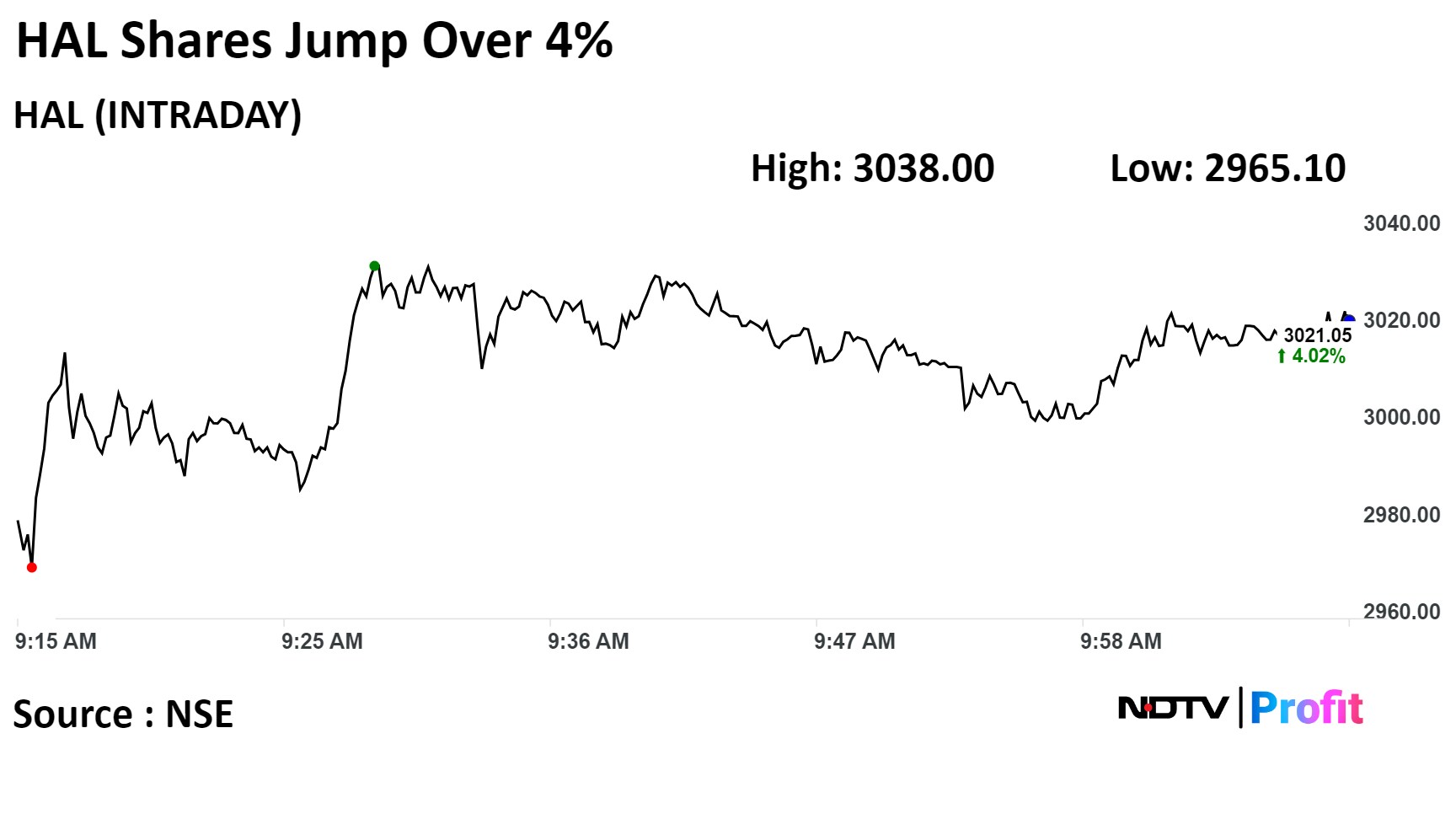

Shares of Hindustan Aeronatics rose as much as 4.61% to Rs 3,038 apiece. It trading 3.89% higher at Rs 3,017.25 apiece as of 10:08 a.m. This compares to a 0.38% advance in the NSE Nifty 50 Index.

The m-cap of the company crosses Rs 2-lakh-crore mark for the first time

The stock Ltd has risen over 370% in the last 12 months. Total traded volume so far in the day stood at 3.6 times its 30-day average. The relative strength index was at 78, suggesting stock may be overbought.

Out of 14 analysts tracking the company, 13 maintain a 'buy' rating, and one suggests a 'sell', according to Bloomberg data. The average 12-month consensus price target implies a downside of 8%.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.