The occasion was the NASSCOM Annual Leadership Summit. The guest was India's richest man and the chairman of Reliance Industries Mukesh Ambani. The proclamation was that data is the new oil and soon data analytics will enable people to obtain loans within 10-15 seconds.

What Ambani predicted is not a distant dream but something that is already happening.

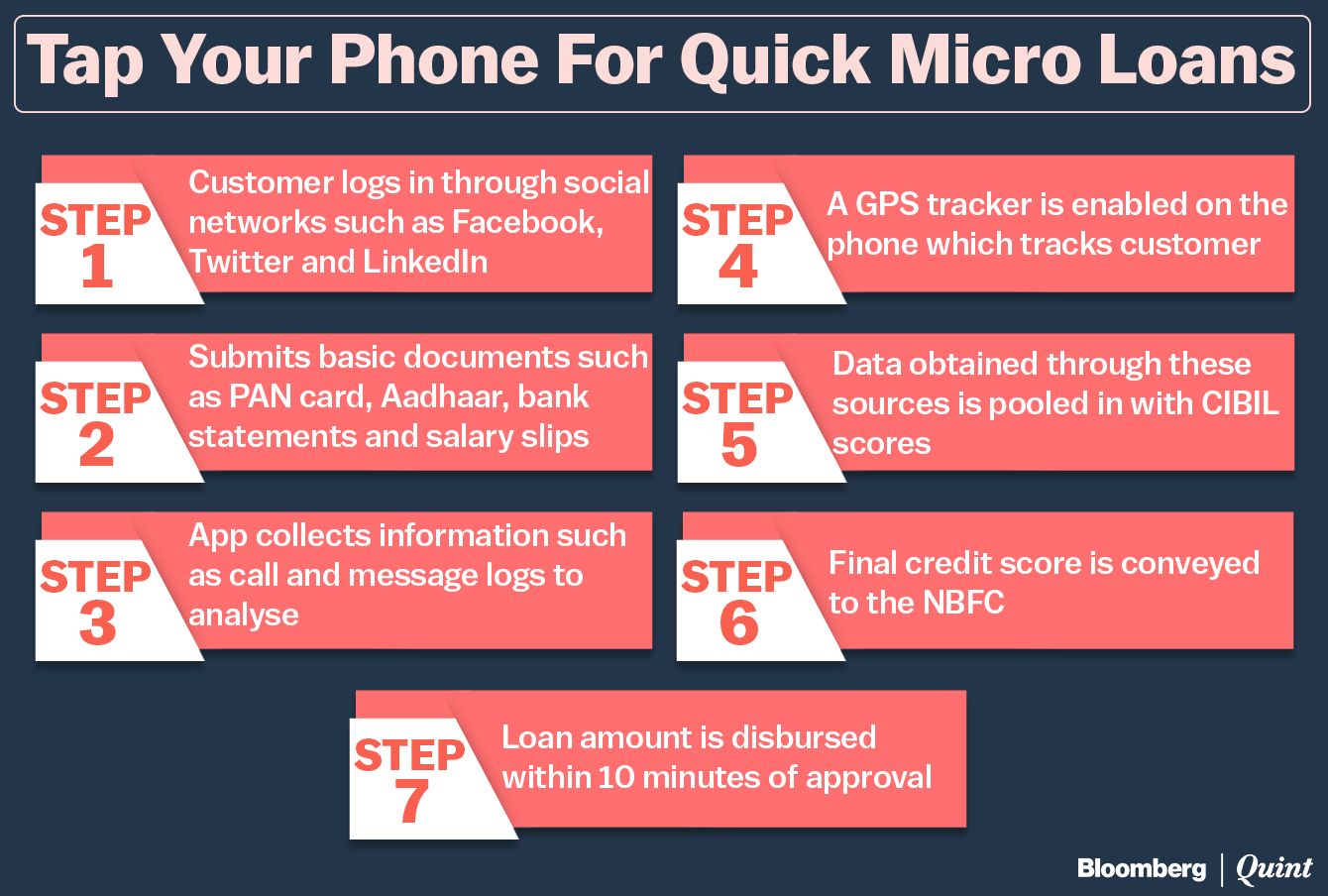

CashE, founded by V Raman Kumar, in April last year provides micro-loans through its mobile app to salaried people in the 22-36 age group based on their financial position as well as social data. The entire process - from application to appraisal and disbursement - is completed with 10 minutes provided all documents are in place, Kumar said in a conversation with BloombergQuint.

The company's target audience is a cohort of 80 lakh young people in the country who are earning more than $3250 or Rs 2.28 lakh per annum. Kumar said that this is a group which will keep expanding, providing a large market for its products. CashE banks on the fact that young people (who don't shy away from spending) may run out of money by the end of the month and may need a little loan till the next paycheck hits the bank account. ‘Payday loans' as they are called.

CashE caters to this need by offering loans between Rs 5,000 to Rs 1 lakh for a tenure of 15, 30 or 90 days. But these loans don't come cheap. 30-36 percent is the rate of interest charged, along with a processing fee. Kumar insists these rates are in line with what credit card companies charge.

Innovation Red Flags?

The concept of payday loans may be relatively recent in India but it has been tried, tested and shunned in some developed markets like the US and UK.

This is known as the payday market and not looked at very kindly by the regulators in the market because of their high interest rates. They serve a purpose because people would otherwise go to informal market where they would pay higher interest rates.Harsh Roongta, Sebi Registered Investment Adviser

Roongta added that there is an added element of risk in a market like India where not enough borrowers have reliable credit scores and a long enough credit history.

To this, Kumar said that the risks are priced into their interest rates and the company is catering to a market which is relatively well off already.

“Banks are trying to get into long term lending. We would like to only go and cater to the immediate short term requirement. This requirement could be a lifestyle need, a family emergency or a medical emergency,” Kumar said while adding that his company has studied the behaviour of millennials and concluded that they don't like to get tied up with long term arrangements or equated monthly installments.

The loans provided by CashE are disbursed off its own balance sheet as the company is registered as a non-banking finance company itself by the name of One Capital.

The company mines borrowers' phones and social network for data points to arrive at a creditworthiness score, which is also matched with traditional sources such as CIBIL scores before arriving at a lending decision. This is done through a mobile app which looks for data from call logs, apps and social networks such as Facebook and LinkedIn.

Kumar said that while LinkedIn works as an “excellent proxy” for someone's creditworthiness, it is often only present in the case of high-income borrowers. In other cases, the company has to rely on networks like Facebook and Twitter to mine data.

“We are not reading messages but just looking at the logs. We also look at the apps installed and uninstalled, GPS location etc which continues to be with us till we have your telephone number,” Kumar said.

The company also asks borrowers to submit crucial documents such as their PAN card, Aadhaar number, bank statements and salary slips online. All these documents are matched with data collected by the company and that provided by CIBIL to arrive at a final decision. The loan amount, if sanctioned, is credited into a customer's bank account within a few minutes.

We can ping into your CIBIL score and look at your existing credit score but your CIBIL score has no bearing on my loan giving process. We are giving uncollateralized loans and all that we want to know is whether someone has the wherewithal and the inclination to pay. Wherewithal we find from the data that people submit and inclination is something we gauge from a bunch of parameters.V Raman Kumar, Chairman, CashE

Asset Quality Track Record

In the initial days, CashE saw delinquencies or non performing assets of upto 11 percent of its total loan book. This, Kumar claims, has come down to 2.5 percent. He said that the predictive engine will become much better as more data is fed into it.

“We can always sell these loans to a collection agency and recover a portion of the money. We have factored all that into our interest rates. We charge a reasonably good interest rate which covers NPAs,” he added.

These high interest rates, however, could impede business growth as customers become more aware of the formal banking system and start availing cheaper credit, said Roongta.

“That [interest rate] becomes a problem because the moment the consumer knows he is paying a high interest rate, he is likely to shy away from taking the loan. The market becomes suspect,” Roongta said.

What's The Growth Potential?

The company claims that it adds about 700 customers a day. It acknowledges that high instances of default in the early days forced it to tighten its processes. About one-fourth of the total applicants get a loan and the company claims that 70 percent of these turn into repeat clients.

While the company operates on an app-only model, it also relies of some external platforms to get clients in. These include tie-ups with postpaid telecom retailers and loan aggregators. These platforms, said Kumar, helps them tap a market that banks have shied away from.

“Banks typically rely on CIBIL score and reject applications even if it's a little lower so that entire lot also comes to us. Most of these are people who need the money and have the qualification to pay it back. They might have a bad CIBIL score which has been tampered by a few instances of bad behaviour in the past,” Kumar said.

Banks tightened processes in the unsecured lending segment, which includes personal loans of the kind that CashE offers, after large instances of default in this segment following the global financial crisis. Since then, banks have been selective around unsecured lending and prefer to lend largely to their own customers.

This report is part of a series profiling fintech firms changing the way financial services operates in the India. The series will play out every weekend on Bloombergquint.com

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.