(Bloomberg Opinion) -- BMW AG Chief Executive Officer Oliver Zipse was incredulous when asked this month whether the German premium carmaker would respond to a brutal price war in electric vehicles by cutting production.

“Do I understand you right that you try to slow us down? Two years ago, it was the other way around,” he told analysts, triggering wry laughter.

Carmakers not called Tesla Inc. have spent the past decade being cajoled by governments, capital markets and journalists like me to speed up the transition to electric vehicles — and for good reason, because the planet is overheating. Now that EV sales aren't growing as fast as anticipated, Volkswagen AG, General Motors Co. and Ford Motor Co. are being forced to either reduce EV output or delay new models and factories. (BMW hasn't cut back, yet.)

It's an agonizing moment for incumbents and new entrants alike; the winners will those able to respond nimbly to volatile consumer demand, while not forgetting that the energy transition is unstoppable. Thanks to a flexible manufacturing system and prior experience of underwhelming EV sales, BMW should be more resilient than most.

Leaving aside enthusiastic early adopters, most consumers haven't yet been persuaded to go electric due to lingering worries about cost, recharging, high insurance premiums and poor residual values. These problems are solvable, but I don't blame customers for having doubts: A car is the second most expensive thing most of us buy, and EVs often aren't affordable.

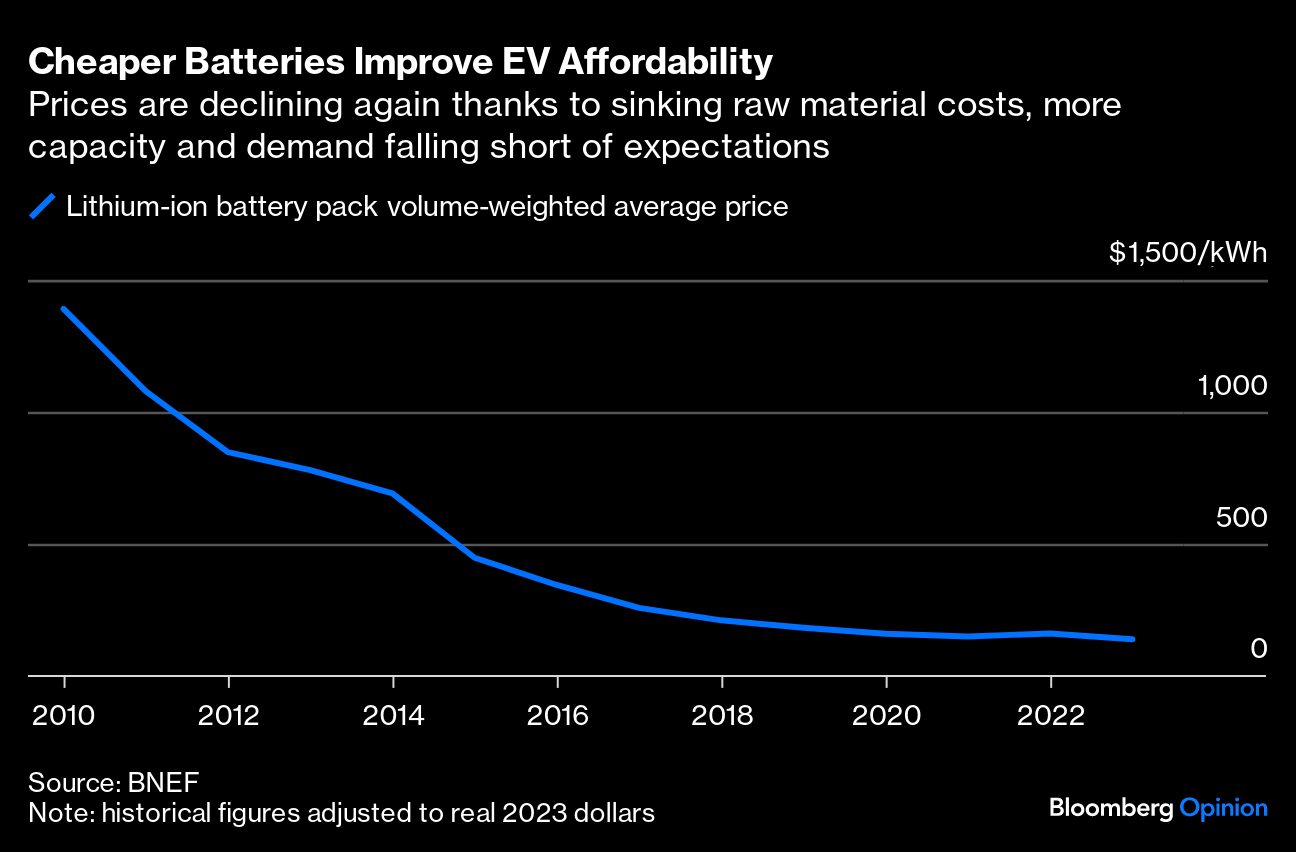

As with mobile phones or televisions , the next generation of battery-powered models will be better value and more capable than the first — and also more profitable for manufacturers. (Ford's EV unit has lost more than $3 billion so far this year)

The crux of the problem, as far as the industry is concerned, is that only by investing more in factories and technology will it achieve the scale economies and lower costs needed to attract more buyers. The sums are astonishing — VW anticipates investing more than €120 billion ($131 billion) in EVs and software in the next five years. Automakers have tried to limit the risks of misjudging demand by entering into battery joint ventures.

President Joe Biden's administration is offering gargantuan subsidies under the Inflation Reduction Act, which have been matched by neighboring Canada. Automakers and battery makers could together receive more than $170 billion toward the cost of running their North American battery plants, according to the sum of Benchmark Mineral Intelligence and Canadian Parliamentary Budget Officer estimates.

In short, automotive capital junkies have become subsidy junkies, but there's a catch: IRA production incentives are scheduled to end in 2032 — that's if Republicans and Donald Trump haven't already scrapped them — hence the flurry of gigafactory announcements seen in the past year.

The capital markets have dictated a similarly rapid transition. Tesla is valued a gazillion times above everyone else because it isn't encumbered by dying combustion engines, and builds EVs profitably. Meanwhile, European automakers are shunned by investors due to concern they'll be swamped by cheap and technologically advanced Chinese EV imports.

A reassessment is now underway. Tesla's profit margins have tumbled this year after price cuts, rising interest rates and insufficient demand for the two electric models that contribute the vast majority of revenue. Meanwhile, China's EV sector is beset by overcapacity.

The US and Europe still need a lot more battery and EV plants, but manufacturers are reviewing the timing of some of that spending — potentially leaving some IRA money on the table. (This is far from a universal trend, however, with others, including Hyundai Motor Co. and Toyota Motor Corp., stepping up the pace of EV investments.)

The answer is not for governments to relax emissions targets, but to use the current hiatus to speed up the rollout of recharging infrastructure.

I have limited sympathy for western automakers. Instead of developing affordable and attractive EVs they spent too long selling gas-guzzling SUVs and trucks and arguing these are what consumers desire. To paraphrase Steve Jobs, it's up to companies to show consumers what they want — as Tesla did.

Citroen's €23,300 e-C3, built in Slovakia and arriving early next year, is exactly the kind of reasonably priced model needed to convince holdouts to get a plug. Plunging battery metal prices are also encouraging for EV cost competitiveness and demand.

A decade ago, BMW broke new ground in EV design with the i3 electric hatchback, but most consumers preferred its gasoline and diesel models and the i3 was discontinued last year. But BMW learned a valuable lesson. Its factories have been redesigned so combustion-engine, electric and hybrid models can be built on the same line, so it can respond flexibly to waxing and waning demand.

Though its target of achieving 50% EV sales by 2030 is much less ambitious than some peers, the Munich-based company has a comprehensive and attractive lineup of battery-powered models. It still needs consumers to buy them — but it looks better positioned than peers to navigate the bumpy road ahead.

More From Bloomberg Opinion:

It's Darkest Before the Dawn in the EV Revolution: David Fickling

Auto Strikes Over, Market Senses Bigger Problems Ahead: Liam Denning

A Two-Speed Electric Car Market Is Heading for a Crash: David Fickling

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies in Europe. Previously, he was a reporter for the Financial Times.

More stories like this are available on bloomberg.com/opinion

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.