After a gap of nearly 26 years, the Indian government is actively considering raising the extent of insurance offered on bank deposits. At present, only Rs 1 lakh in deposits is insured, irrespective of how much you hold in an account.

The recent failure of Punjab & Maharashtra Cooperative Bank, where the Reserve Bank of India has imposed restrictions on deposit withdrawals, has forced a rethink on the issue of deposit insurance. On Friday, Finance Minister Nirmala Sitharaman said the government is likely to raise the deposit insurance amount. She declined to give specific details on the extent to which deposit insurance would be raised.

Determining The Correct Cover

The insurance cover of Rs 1 lakh has been in place since 1993. This is paid out in the event that a bank is liquidated.

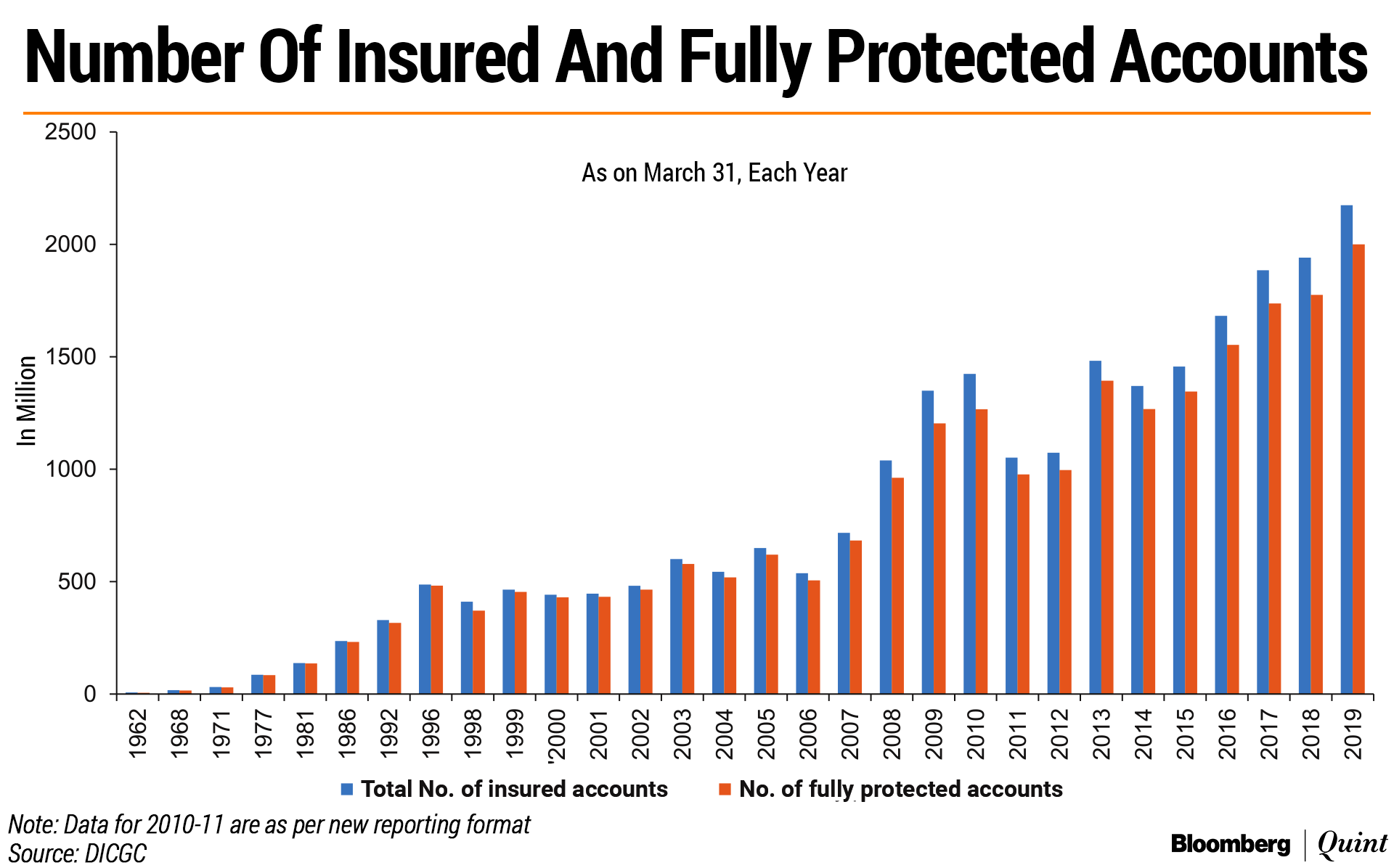

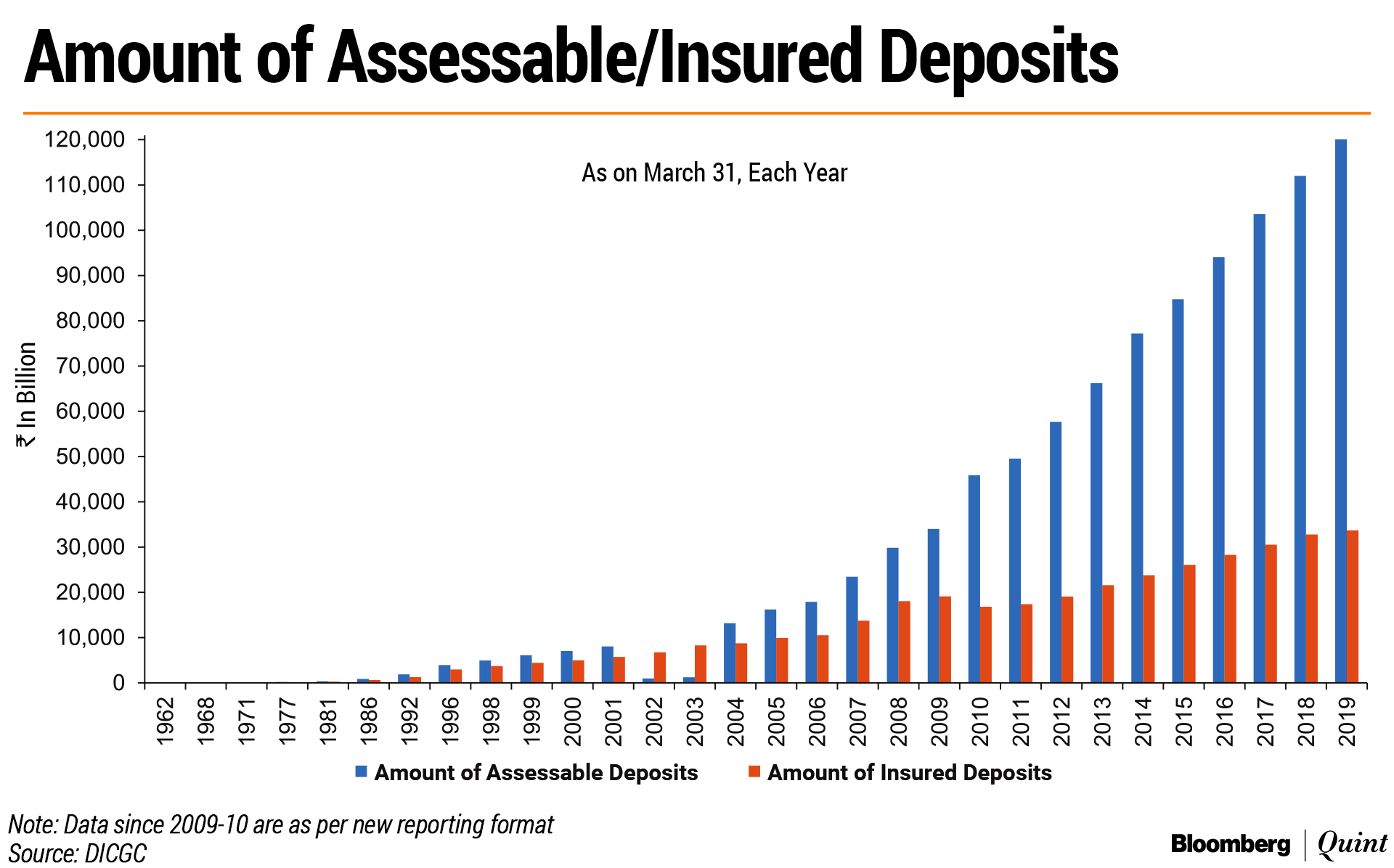

Between 1993 and 2019, as the base of deposits across the Indian banking system has increased, the extent of protection has changed. The number of fully protected accounts is still high at 92 percent. However, the proportion of deposits protected has come down to 28 percent as of March 2019.

Raising the deposit insurance would ensure that a greater proportion of deposits is protected.

What would be the benchmarks used to decide on the level of insurance? There are no clear internationally accepted standards but experts believe that the decision could be guided one of the following benchmarks:

- The International Association of Deposit Insurers, of which India's Deposit Insurance Corporation is a member, recommends a minimum coverage of 80 percent of all accounts and 20-30 percent of all deposits by value. India, even at the current level of insurance, meets that mark.

- However, other benchmarks that can be used include per capita income, where it is suggested that deposit insurance cover should be double of the per capita income, which, in India's case, stood at Rs 1,42,719 in 2018-19.

- Another way would be to use inflation indices to assess the required increase in deposit cover over a certain period, in this case between 1993 and 2019.

According to Anand Sinha, former deputy governor, RBI, “there is a case for raising the deposit insurance limit, but it needs to be balanced so that 100 percent of all deposits are not guaranteed. At the same time the government would want to cover a reasonable amount of deposits.”

What this means is that the new insurance limit should cover the bulk of small depositors in the banking system at present, Sinha told BloombergQuint, as in advanced economies there are social security programs that small depositors can rely on at all times, whereas Indians do not have the same.

While the government has not declared the revised insurance cover for bank deposits, Sahakar Bharati, a non-governmental organisation representing over 20,000 co-operative societies, has recommended that the deposit insurance limit for individual accounts be raised to Rs 5 lakh and for institutional depositors it should be raised to Rs 25 lakh.

Funding The Increased Insurance Cover

Since 2005 banks have been paying a flat-fee premium rate of 10 paise for every Rs 100 worth of deposits, to maintain an insurance cover of Rs 1 lakh per depositor. Should the extent of insurance be raised, banks would have to increase the premium payment, which would eventually be passed on to customers in some form.

A debate has erupted on whether each bank should be asked to pay the same premium or whether banks seen to be at a higher risk of failure should be asked to pay more? An RBI committee in 2015 had suggested differential premium for banks based on their risk profile.

At its meeting last month, the central board of the RBI directed the Deposit Insurance and Credit Guarantee Corporation of India to create a risk-based framework for premium collection from banks, said a person familiar with the matter who spoke on condition of anonymity. Banks should pay their premiums to DICGC based on their financial position, this person said.

Some economists agree.

“Flat-rate premium systems are also unfair in practice as low-risk banks are required to pay the same premium as higher-risk banks. Thus, with no incentive for higher risk banks to improve their risk profile it introduces an element of moral hazard in the system and perpetuates the same,” said Soumya Kanti Ghosh, group chief economist, State Bank of India in report dated Nov. 5.

Increasing the premium rate across the board could also result in a moral hazard, said Madan Sabnavis, chief economist, Care Ratings. “There have been no significant claim payouts made by the DICGC in recent years. If this continues then banks can question the DICGC why they should pay the higher premium rate when the risk of failure is low,” he said.

Determining the embedded risk in a bank is, however, easier said than done.

The 2015 RBI committee had debated how a 'predictive' model could be designed to ensure an accurate assessment of the level of risk associated with each bank. “The Committee felt that such an assurance could be derived only from forward looking inputs into the model; qualitative indicators, being some of them,” the report said.

The committee eventually concluded that a model could be established where about 90 percent weightage is given to parameters based on published data and remaining 10 percent is assigned to other information, including market intelligence on aspects such as internal processes and controls.

Differential premium could also hurt weaker banks, both by sending a signal to depositors and also due to the higher premium payment imposed.

Sinha said that the government and regulator will need make some moderation in the premium pricing for co-operative banks, especially those that are weaker and have a higher insurance premium liability, to ensure the financial impact is minimised.

R Gandhi, former deputy governor at the RBI, however, said that increasing deposit insurance is not likely to affect co-operative banks adversely. “Rather they will be the primary beneficiaries. If premium is linked to risk, then risky coops will have to pay higher premium but it will still be beneficial to them, as the insurance will give confidence to their depositors,” he said.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.