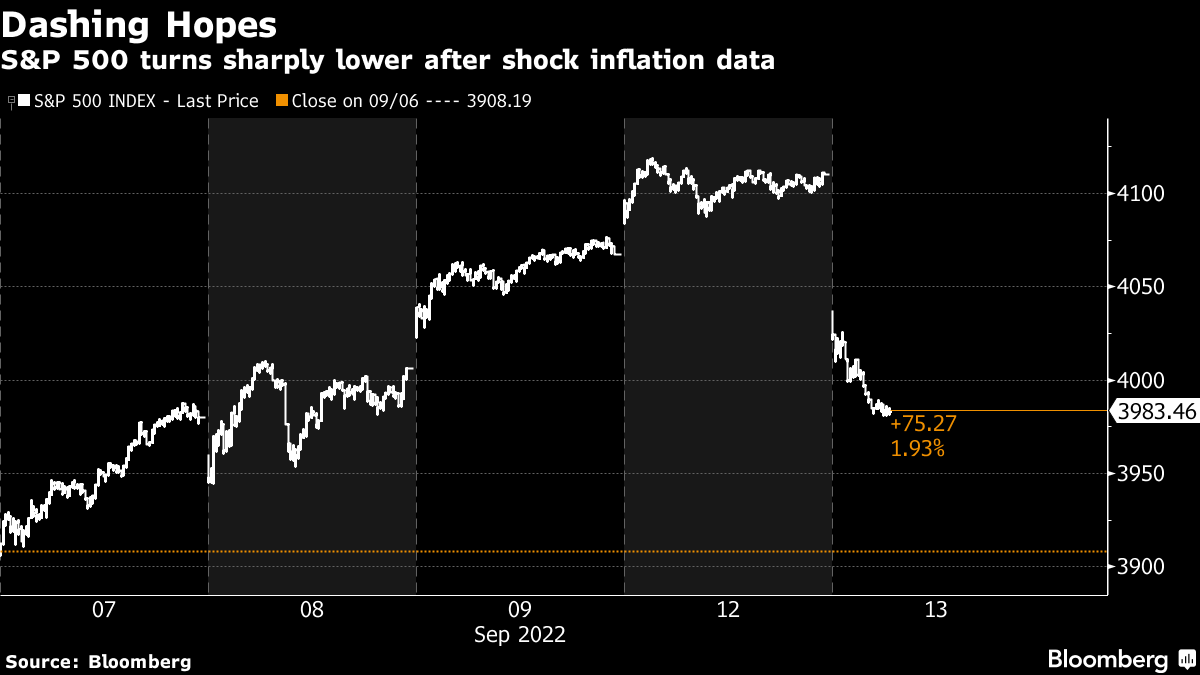

(Bloomberg) -- US stocks extended losses and Treasury yields spiked higher after hotter-than-expected inflation data fueled bets on a jumbo rate hike by the Federal Reserve next week.

A broad-based selloff gripped equities, with S&P 500 falling 3% and the-heavy Nasdaq 100 sinking more than 4% as yield-sensitive stocks took the biggest hit. Swaps traders are now fully pricing in a rate increase of three-quarters of a percentage point, with wagers rising for moves in November and policy rates ultimately reaching around 4.3% early in 2023.

Read more: ‘Wrong-Footed' Traders Confront Prospect of Even Bigger Fed Hike

The two-year Treasury yield, the most sensitive to policy changes, jumped as much as 21 basis points, pushing it more than 30 basis points above the 10-year rate and deepening an inversion in what is generally a recession warning.

The consumer price index increased 0.1% from July, after no change in the prior month, Labor Department data showed Tuesday. From a year earlier, prices climbed 8.3%, a slight deceleration but still more than the median estimate of 8.1%. So-called core CPI, which strips out the more volatile food and energy components, also topped forecasts.

Read more: Biggest Jump in US Rents Since 1991 Keeps Overall Inflation High

“The recent bounce in equities looked incredibly ill-judged and premature,” said James Athey, investment director at Abrdn. “That CPI number is very strong relative to consensus and will not be what the Fed wanted to see at all. The chance of the pace of hikes slowing after September has receded somewhat as a result of this data.”

More comments

- “Headline inflation has peaked but, in a clear sign that the need to continue hiking rates is undiminished, core CPI is once again on the rise, confirming the very sticky nature of the US inflation problem,” Seema Shah, chief global strategist at Principal Global Investors, said in a note. “In fact, 70% of the CPI basket is seeing an annualized price rise of more than 4% month-on-month. Until the Fed can tame that beast, there is simply no room for a discussion on pivots or pauses.”

- “The CPI report was an unequivocal negative for equity markets,” wrote Matt Peron, director of research at Janus Henderson Investors. “The hotter than expected report means we will get continued pressure from Fed policy via rate hikes. It also pushes back any “Fed pivot” that the markets were hopeful for in the near term.”

- “Although today's announcement shows that inflation remains historically high, there may be signs that the pressure of inflation is abating,” said Richard Flynn, managing director of Charles Schwab UK. “Company inventories are rising relative to sales, global economic growth has weakened, and the U.S. dollar is strong -- all indications that price hikes may begin to slow soon. That being said, inflation is still far-above the Fed's target.”

- “While there has been some easing in long-term inflation expectations, recent data still overall point to a picture of high inflation and a tight labour market,” said Silvia Dall'Angelo, a senior economist at Federated Hermes Ltd. “This implies the risk of inflation becoming entrenched via second-round effects is still elevated. Accordingly, the Fed will likely stick to its hawkish trajectory in the coming months.”

- “I'd buy this dip,” said Peter Tchir, head of macro strategy at Academy Securities. “There are bigger issues facing us, but this seems like an algo driven response to the data, chasing out recent weak longs, so I'm a buyer of stocks and bonds here.”

The latest inflation data came amid debate about the outlook for the global economy and how that will affect markets. Stocks have rallied in recent days, with the S&P 500 completing its biggest four-day surge since June on Monday. JPMorgan Chase & Co. said a soft landing is becoming the more likely scenario for the global economy, but Bank of America Corp.'s latest survey showed the number of investors expecting a recession has reached the highest since May 2020.

A gauge of the dollar reversed a decline to trade 0.9% higher. The rally in crude oil stalled as the dollar's ascent offset global demand concerns. Bitcoin fell below $22,000.

What's your dollar bet ahead of the Fed decision? This week's MLIV Pulse survey asks about the best trades ahead of the FOMC meeting. Please click here to share your views anonymously.

Here are some key events to watch this week:

- UK CPI, Wednesday

- US PPI, Wednesday

- US business inventories, empire manufacturing, retail sales, initial jobless claims, industrial production, Thursday

- China home sales, retail sales, industrial production, fixed assets, surveyed jobless rate, Friday

- Euro area CPI, Friday

- US University of Michigan consumer sentiment, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 fell 3% as of 1:03 p.m. New York time

- The Nasdaq 100 fell 4.1%

- The Dow Jones Industrial Average fell 2.7%

- The MSCI World index fell 2.5%

Currencies

- The Bloomberg Dollar Spot Index rose 1%

- The euro fell 1.2% to $1.0002

- The British pound fell 1.3% to $1.1527

- The Japanese yen fell 1% to 144.27 per dollar

Bonds

- The yield on 10-year Treasuries advanced seven basis points to 3.42%

- Germany's 10-year yield advanced eight basis points to 1.73%

- Britain's 10-year yield advanced nine basis points to 3.17%

Commodities

- West Texas Intermediate crude fell 2.1% to $85.96 a barrel

- Gold futures fell 1.5% to $1,714.90 an ounce

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.