The Indian stock market hit a record high in November 2022 and the momentum continued in December as well. However, things have changed in the past few days.

Markets have fallen amid concerns over rising Covid cases globally. Moreover, apprehensions ahead of Reserve Bank of India's latest policy meet and key macroeconomic data from the US have also contributed to the fall.

While these short-term concerns may continue to affect the markets, it may be a good opportunity to enter the market to scout best midcap stocks for the long-term.

Here are ten undervalued midcap stocks to watch out for in 2023.

#1 DCM Shriram

First on our list is DCM Shriram.

DCM Shriram's share price has shot up in the past five years, rewarding its shareholders with a 50 per cent return. However, since the beginning of the year, the share price is down 10 per cent.

It is trading at a Price-to-Earnings ratio (P/E) of 12.1 times, a mere 17 per cent premium to its 5-year median P/E of 10.2 times.

DCM Shriram is conglomerate. It runs a wide array of businesses, ranging from chemicals and agricultural products to sugar and cement.

While chemicals and agricultural products contribute equally to the business with over 51 per cent of the revenues, sugar contributes over 40 per cent, with balance coming from other cement and other smaller businesses.

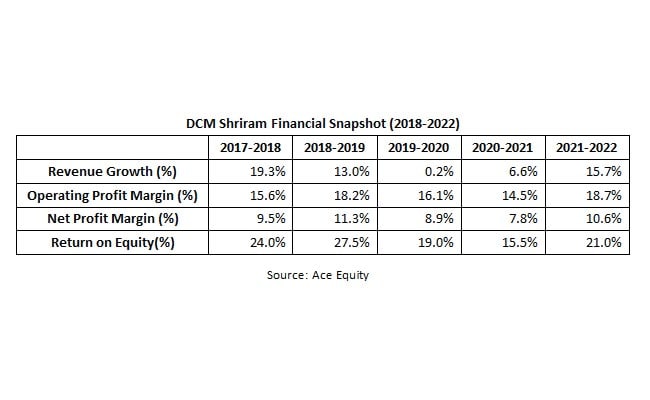

DCM Shriram Financial Snapshot (2018-2022)

The company has grown its business substantially in the past few years. While the sales have grown at a 5-year compound annual growth rate (CAGR) of 10.6 per cent, the net profit has grown at 14.1 per cent.

This outstanding performance has resulted in high return ratios, enabling the firm to retain a solid balance sheet. The 5-year average return on equity (RoE) stands at 21.4 per cent, and the debt-to-equity ratio is low at 0.27 times.

#2 Gujarat Ambuja Exports

Next on our list is Gujarat Ambuja Export.

Gujarat Ambuja Export's stock price is up 1.6 times in 5 years and 46 per cent since the beginning of the year. Despite this, the stock trades at a PE of 13.3 times, a 14 per cent premium to its 5-Yr P/E.

The company is principally involved in the agro-processing business with dominance in maize products, edible oils, and cotton yarns.

It competes in the domestic and global markets and caters to the food, pharmaceutical, and feed industries. It has 12 manufacturing facilities spread across India and exports to over 75 countries.

The maize processing and edible oil segments are the key growth-driving factors contributing to its presence in the domestic market. While the maize processing unit contributes 56 per cent to the total revenues, the edible oil unit contributes 38 per cent.

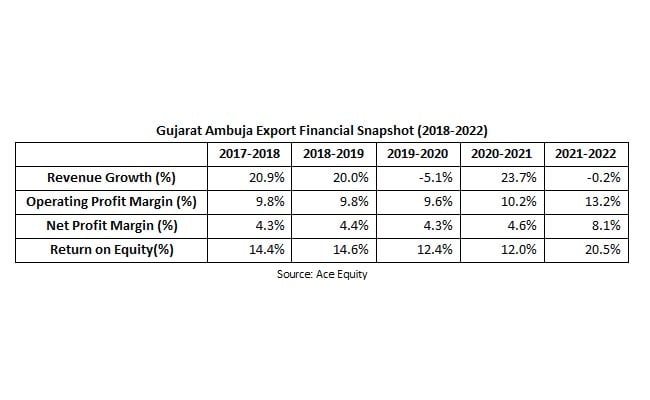

Gujarat Ambuja Export Financial Snapshot (2018-2022)

The dominant position has allowed the business to perform well over the past few years. The sales has grown at a 5-year CAGR of 8.4 per cent while net profit has grown at a CAGR of 33.7 per cent respectively.

This has expanded the RoE to 25 per cent in the financial year 2022 from 15 per cent in 2018, and helped the company maintain a healthy balance sheet with negligible debt.

#3 Transport Corporation Of India

Third on our list is the Transport Corporation of India (TCI).

The stock price has doubled in the last five years. However, it has fallen by over 14 per cent since the beginning of the year. It is now trading at a P/E ratio of 15.3 times, a 12 per cent discount to its 5-year average of 17.4 times.

TCI is the country's premier organised freight services provider with a pan-India presence. The company offers Integrated logistics & supply chain solutions catering primarily to the healthcare, auto, chemicals, and retail industries.

It enjoys a wide presence across segments such as coastal shipping services, container & bulk cargo movements, and rail and road transportation services.

This integrated offering allows it to offer last-mile connectivity, setting it apart from other players. And the company's performance in the past few years is a true testament to that.

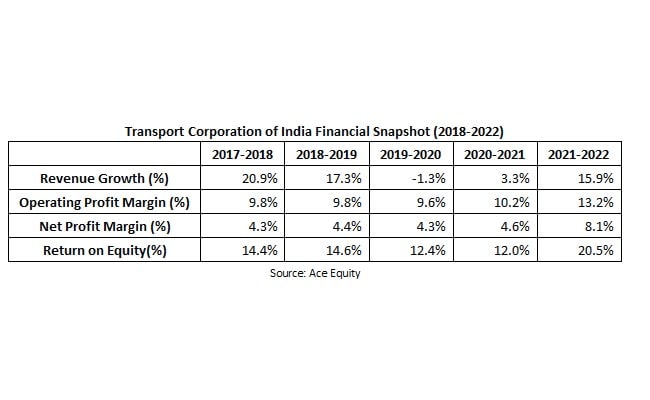

Transport Corporation of India Financial Snapshot (2018-2022)

While the sales have registered a 5-year CAGR of 10.9 per cent, the net profit has grown by 32.1 per cent. This has led to strong returns with a 5-year average RoE of 14.8 per cent. The company enjoys a pristine balance sheet with a 0.36 times debt to equity.

#4 Eris Lifesciences

Fourth on our list is Eris Lifesciences.

The company's stock price has been falling since the beginning of the year. It has tumbled over 13 per cent. It is trading at a PE of 23 times, a 6.5 per cent discount to its 5-year median PE of 24.6 times.

Eris is a pharmaceutical company. It derives its revenue from the domestic branded formulations market, with chronic and sub-chronic therapies accounting for a considerable portion (93 per cent) of the business.

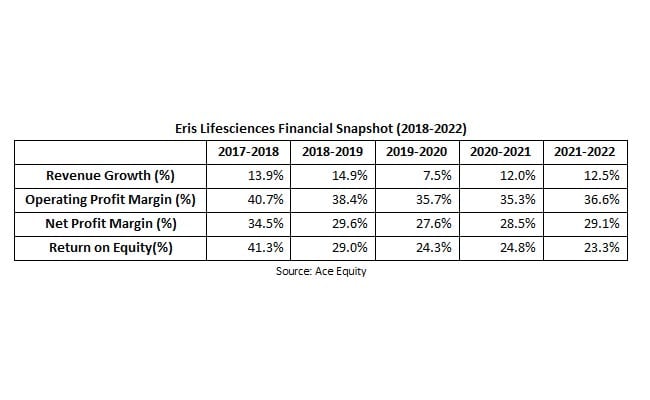

Eris Lifesciences Financial Snapshot (2018-2022)

Their strong and sustainable brands have enabled them to expand their business and operate at high margins. While the sales have grown at a 5-year CAGR of 13.2 per cent, the net profit has grown at 10.5 per cent.

The RoE has also advanced, reporting a 5-year average of 28.5 per cent. This performance has allowed the company to maintain a solid balance sheet and keep the debt levels low.

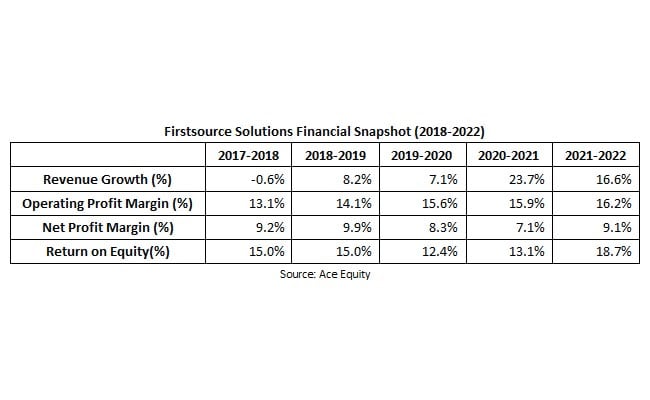

#5 Firstsource Solutions

Fifth on our list is Firstsource Solutions.

The company's stock hasn't performed well since the beginning of the year, affected by the fears of a global recession. It is down 32 per cent, trading at a PE of 15 times, just a 9 per cent premium to its 5-year median PE of 13.7 times.

Firstsource is an information technology (IT) company catering primarily to the banking, financial services and insurance (BFSI) (43 per cent of the total revenues), healthcare (34 per cent), communication and media industries (20 per cent).

The company boasts a well-diversified stream of revenues, with the top five clients accounting for 35 per cent of the business.

Firstsource Solutions Financial Snapshot (2018-2022)

In recent years, the business has risen significantly. On a 5-year CAGR basis, the sales and net profit have reported 10.7 per cent and 14 per cent growth. The returns have been robust, expanding the RoE from 15 per cent in the financial year 2018 to 18.7 per cent in 2022.

Much like its peers, the company has funded this growth with negligible debt on its book. The debt-to-equity ratio in the financial year 2022 stands at 0.35 times.

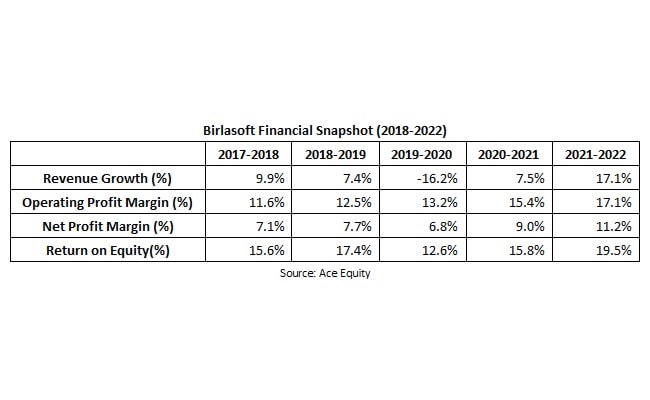

#6 Birlasoft

Next on our list of undervalued midcaps is Birlasoft.

The stock has not been immune to the fears of a global recession affecting the entire IT sector adversely. The stock price has fallen by over 35 per cent since the beginning of the year. It is now trading at a PE of 17 times, a 21 per cent premium to its historical median PE of 14 times.

Birlasoft is an information technology (IT) company catering primarily to manufacturing (46 per cent of total revenues), pharmaceutical (22 per cent), banking, financial services and insurance (BFSI) (17 per cent), energy and utility (15 per cent) sectors.

The company boasts a well-diversified stream of revenues, with the top five clients accounting for 30 per cent of the business.

A large part of the business comes from the USA, which accounts for nearly 80 per cent of the total revenues, followed by Europe (11 per cent) and the rest of the world (9 per cent).

Birlasoft Financial Snapshot (2018-2022)

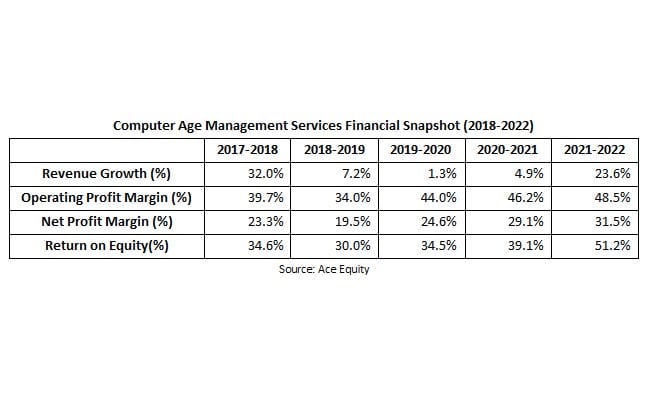

#7 Computer Age Management Services

Seventh on our list is Computer Age Management Services (CAMS).

The company's stock price has fallen over 15 per cent since the beginning of the year. It is now trading at a PE of 39 times, a 13 per cent discount to its 5-year median PE of 45 times.

CAMS is the largest registrar and transfer agent of the Indian mutual fund industry.

The company enjoys an aggregate market share of 69.5 per cent of the assets under management with mutual funds. Its mutual fund customer list boasts ten of the country's top fifteen largest mutual funds.

Their primary job is to deliver a seamless interface to asset management companies, investors, exchanges, depositories, and other stakeholders.

Computer Age Management Services Financial Snapshot (2018-2022)

CAMS's dominance in the business has contributed to the robust growth reported by the company in recent years. The sales and net profits have reported a 5-year CAGR of 13.7 per cent and 17.7 per cent, respectively.

The RoE has also expanded, up from 33 per cent in the financial year 2018 to 46 per cent in 2022. With a debt-free balance sheet in tow, the business is all set to benefit from the fintech megatrend.

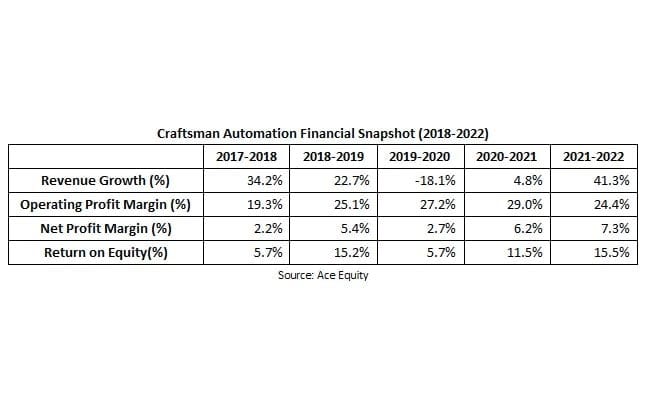

#8 Craftsman Automation

Eighth on our list is Craftsman Automation.

The company's stock price is up 45 per cent since the beginning of the year, mainly led by the demand uptick in the auto segment.

Despite this outperformance, it is trading at a PE of 35 times, a mere 10 per cent premium to its 5-year median of 31.8 times.

Craftsman Automation operates in three main segments largely catering to the automobile sector. These include automotive powertrain (52 per cent of the revenue mix), automotive aluminium (20 per cent), and industrial & engineering (28 per cent).

The company is a leading player in the machining of critical engine and transmission components, primarily for medium and heavy commercial vehicles (MHCVs), tractors and off-highway segments. However, its relatively new aluminium die-casting business has also taken off.

Craftsman Automation Financial Snapshot (2018-2022)

This is evident from the growth reported by the company in recent years. The sales and net profits have grown at a 5-year CAGR of 12.9 per cent and 30.9 per cent. This comes on the back of margin expansion and growth in volume, leading to an improvement in returns.

While the RoE went up from 5.5 per cent in the financial year 2018 to 14 per cent in 2022, the debt-to-equity ratio went down from 0.7 times to 0.3 times over the same period.

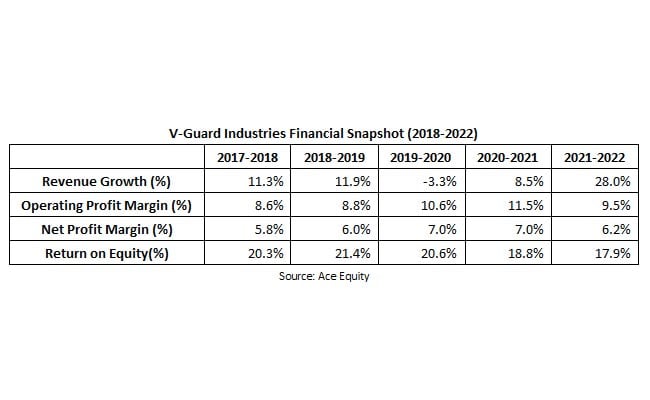

#9 V-Guard Industries

Next up is V-Guard Industries.

The company's stock is up 20 per cent since the beginning of the year. Despite the jump, it is trading at a PE of 48 times, a discount to its historical 5-yar PE of 52 times.

V-Guard Industries is an electronics manufacturer operating in the capital goods sector. The business comprises electronics (23.5 per cent of total revenues), electricals (45.9 per cent), and consumer durables (30.6 per cent).

The company's innovative techniques in tandem with an extensive network of distributors have spurred business growth.

V-Guard Industries Financial Snapshot (2018-2022)

While the sales have registered a 5-year CAGR of 11.7 per cent, the net profit has grown by 9.6 per cent. The company has no debt on its books and the 5-year average RoE stands at 19.8 per cent.

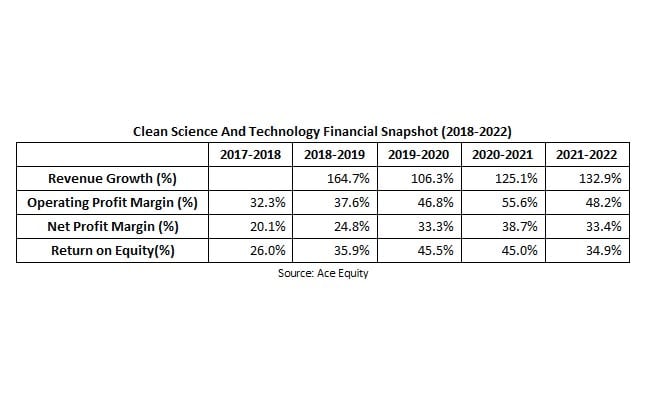

#10 Clean Science And Technology

Last on our list is Clean Science And Technology.

The company's stock price has tumbled around 40 per cent and is trading at a PE ratio of 60 times, which is a 40 per cent discount from its 1.5 year median PE of 86.7 times.

Clean Science and Technology is a leading chemical manufacturer. It manufactures and supplies chemicals to customers across the world. This includes China (35 per cent of total revenues), India (30 per cent), Europe (15 per cent), America (14 per cent), and the rest of the world (6 per cent).

The company is one of the few companies to successfully commercialise environment-friendly processes to manufacture certain speciality chemicals.

Clean Science And Technology Financial Snapshot (2018-2022)

In recent years, the business has expanded significantly. The revenues and net profit have multiplied by more than 3 times in the past 5 years. With no debt on its books, the healthy cashflows have led to 5-year average RoE stands at 37 per cent.

In conclusion

As attractive as smaller undervalued companies may seem, you must understand that the prospect of outsized returns comes in tandem with high volatility.

However, investing for the long term can take care of that. Apart from helping you ride out any short-term market swings, it can also give undervalued businesses enough time to realise their full potential.

Small businesses are more agile and have more room to grow in comparison to their larger peers. Moreover, some midcaps trade at lower prices and valuations, offering the potential for higher returns. So once the company grabs a great opportunity, the business can quickly get on the fast track to growth.

But no matter how great the returns maybe, you must do your due diligence and in-depth research before parting with your hard-earned money.

Happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com.

(Except for the headline, this story has not been edited by NDTV staff and is published from a syndicated feed.)

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.