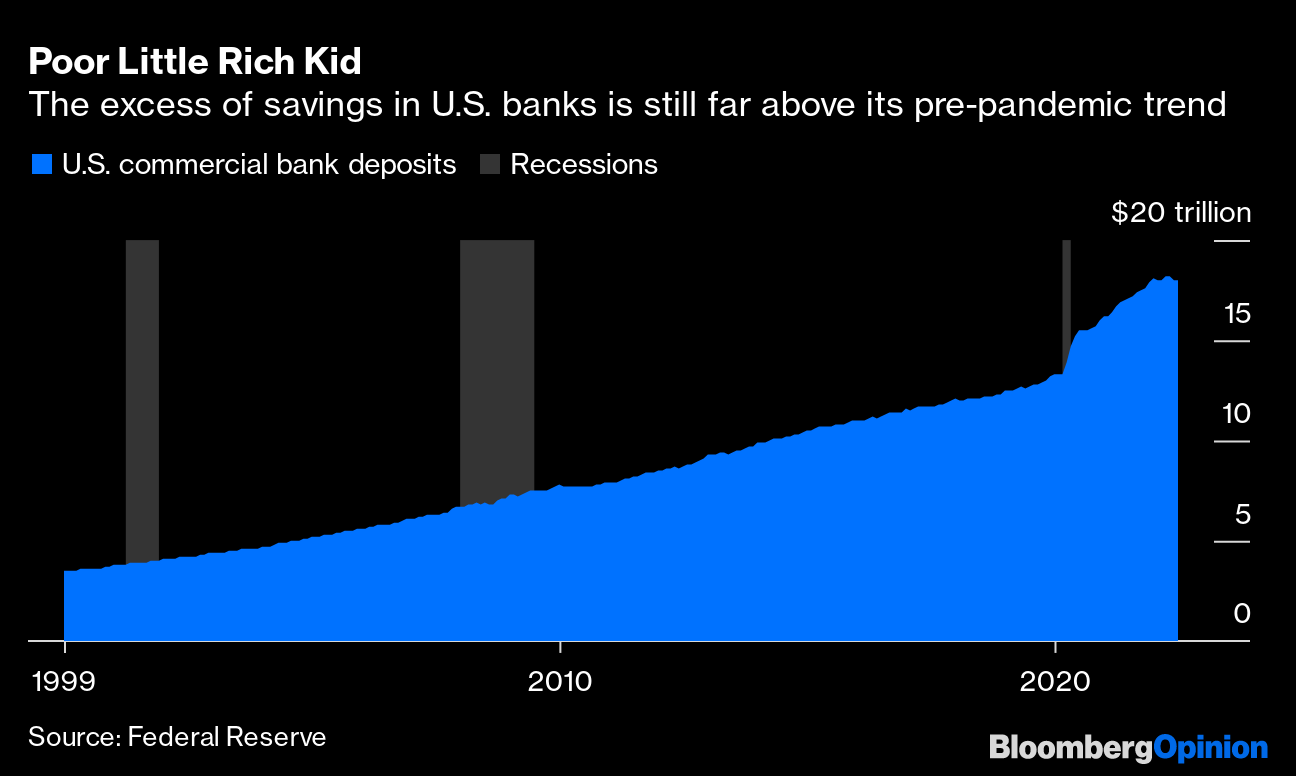

(Bloomberg Opinion) -- Much of the rich world is emerging from two years of pandemic more flush than it's ever been. Deposits held by consumers at U.S. commercial banks are roughly $3.5 trillion above where they'd have been if they continued the pre-pandemic trend, a position that inflation is only starting to eat away.

For the airline industry, it's precisely the opposite. While travel volumes are returning to something like normality in most of the world, the legacy of Covid — in the form of the vast debts clocked up during two years on life support — has barely shifted. If you're looking for an explanation for the chaotic scenes of cancelled flights, lost baggage and passenger number caps at airports this northern hemisphere summer, it's worth considering the drastic cost-cutting the industry will be undergoing for many years to come.

Airlines would dearly love to tempt passengers back with the promise of a return to business as usual. The stubbornly persistent debts they're holding make that almost impossible.

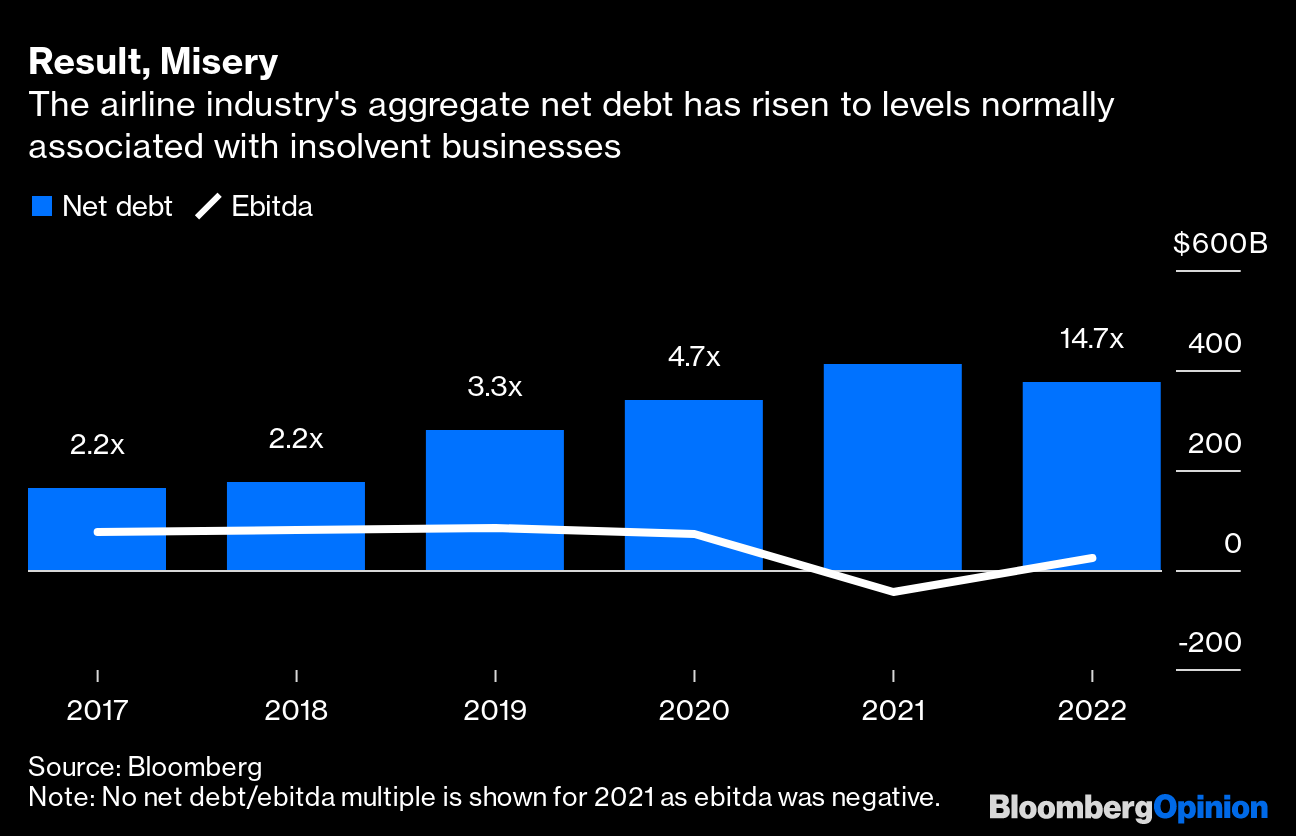

Net borrowings by more than 100 airlines globally for which Bloomberg has data were running at a combined $377.85 billion in their latest reports, more than a third higher than $281.03 billion at the same time in 2019 — and that was already a rough year for the aviation industry, thanks to rising costs and trade tensions. Compared to 2018, debts have doubled.

While traffic volumes are starting to recover, profits are not. Earnings before interest, tax, depreciation and amortization over the past 12 months across the industry amounted to $25.77 billion — an improvement on the $45.98 billion ebitda loss a year earlier, but barely more than a third of typical levels going into the pandemic.

The relationship between those two figures is a decent benchmark for a company's ability to service its debts. Right now it's a flashing red emergency sign.

Banks start to get worried when their corporate borrowers have debts amounting to more than three or four times their ebitda. That number went to 4.7 this time two years ago, before heading off the charts last year when ebitda turned negative. This year, it's worse than it was in 2020, at 14.7 — almost unimaginable levels for any solvent company, let alone an entire industry. Of 113 companies for which Bloomberg has the relevant data, just 23 are able to meet their interest payments out of earnings before interest and tax.

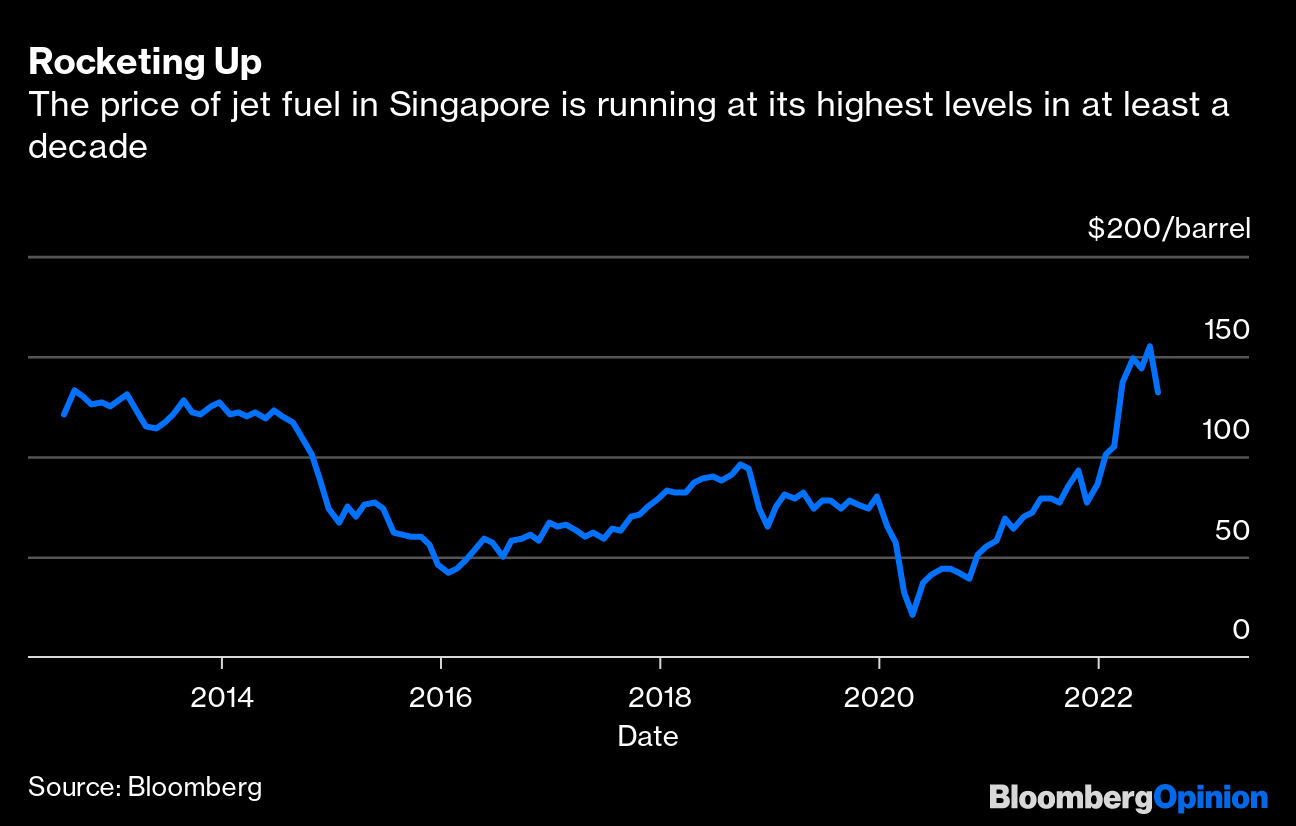

Those numbers may well get worse before they get better. Jet fuel prices, which typically make up 20% to 30% of costs for airlines, are about 50% above their 2019 levels, at $132.31 a barrel in Singapore. Last month, they hit an all-time high of $164.30.

Although net debt levels are down marginally since peaking midway through last year, the cost of servicing those loans has also ballooned as interest rates have climbed. On a very rough estimate taken from the yield on 10-year U.S. government bonds, airlines' interest bill this year is almost double what it was 12 months ago, despite an 8.4% reduction in borrowings.

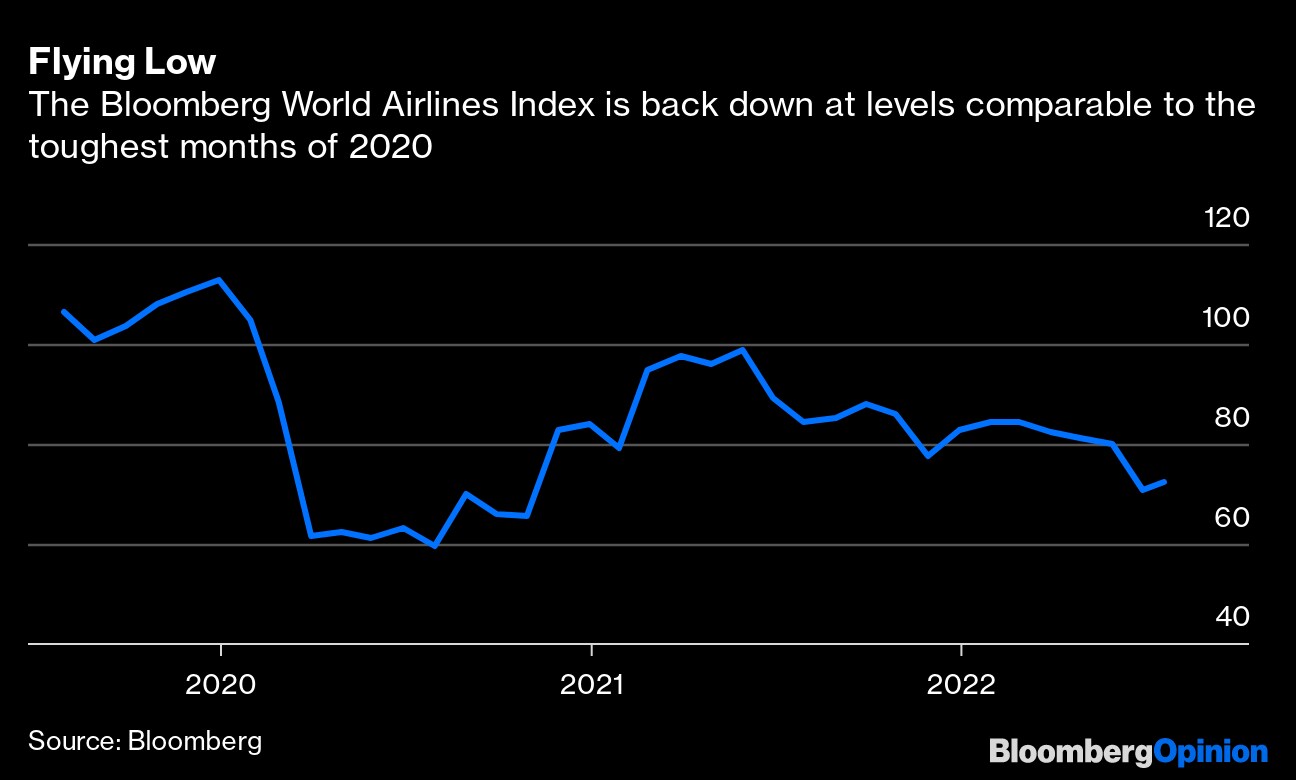

Investors have taken notice. The Bloomberg World Airlines Index, a share-price tracker which staged a remarkable recovery in the year through March 2021, has been trending down ever since. It's currently at levels comparable to the darkest months of the pandemic.

The travel chaos is best understood as an outcome of airlines struggling to rein in the few costs they can control. Around half of the world's nearly 500,000 baggage handlers were put out of work in the early months of the pandemic, and tight labor markets ever since have made it hard to tempt people back to such low-wage, low-security jobs. That's been made worse by the fact that we appear to be focusing our travel more than ever on peak periods, when the pressure on ground services is highest.

Airlines can also save money if they cram the passengers from three flights due to fly one-third empty into two planes, one reason many have been trimming their schedules and cancelling more departures than usual.

Passengers will always end up blaming their travel misery on airlines, but all the problems being experienced right now are the result of an industry that's still fighting to survive after two years in limbo. The chaos at baggage carousels and security lines won't improve until airports see their cashflows recover, which in turn depends on the carriers who contribute the biggest chunk of their revenues chipping away at their own debt piles. At a time when inflation is picking up everywhere, global passenger yields — the amount of money made for flying each passenger one kilometer — are still likely to end the year at roughly the same level as they were in 2019, around seven cents or so.

The problem in the airline industry isn't that it's profiteering from our misery. It's that we're still not prepared to pay for the service we want. Until airlines and airports work off Covid's debt overhang, that situation is unlikely to change.

More From Bloomberg Opinion:

- Beleaguered US Airline Passengers Deserve a Bill of Rights: Brooke Sutherland

- Good Luck Making It to Your Vacation This Summer: Andrea Felsted

- Flying Was Already Hellish. Now It's Worse: Chris Bryant

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering energy and commodities. Previously, he worked for Bloomberg News, the Wall Street Journal and the Financial Times.

More stories like this are available on bloomberg.com/opinion

©2022 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.