(Bloomberg Opinion) -- To hear overseas oil executives talk, you would think that Chinese drivers and air passengers were coming to the rescue of an oil market looking for direction.

Reports from staff on the ground in China suggest that “demand is looking very good,” Trafigura Group Chief Executive Officer Jeremy Weir told Bloomberg Television earlier this month on the sidelines of the CERAWeek industry conference in Houston. “Shops are full, restaurants are full, and I think we're going to see international travel increase a lot.” Downgrades to the outlook for electric vehicles have been serious enough that oil consumption won't peak until the 2030s, Vitol SA CEO Russell Hardy said at the same event.

The group that gives least credence to this bullish talk is a surprising one: oil executives from, er, China.

Electric vehicles will displace more than 20 million metric tons of crude demand this year, equivalent to 10% of the country's gasoline and diesel consumption, according to Lu Ruquan, president of state-owned China National Petroleum Corp.'s Economics & Technology Research Institute. The same 20-million-ton figure was echoed by Dong Zhao, CEO of the biggest refiner, China Petroleum & Chemical Corp. or Sinopec, who predicts Chinese demand won't grow beyond 2026.

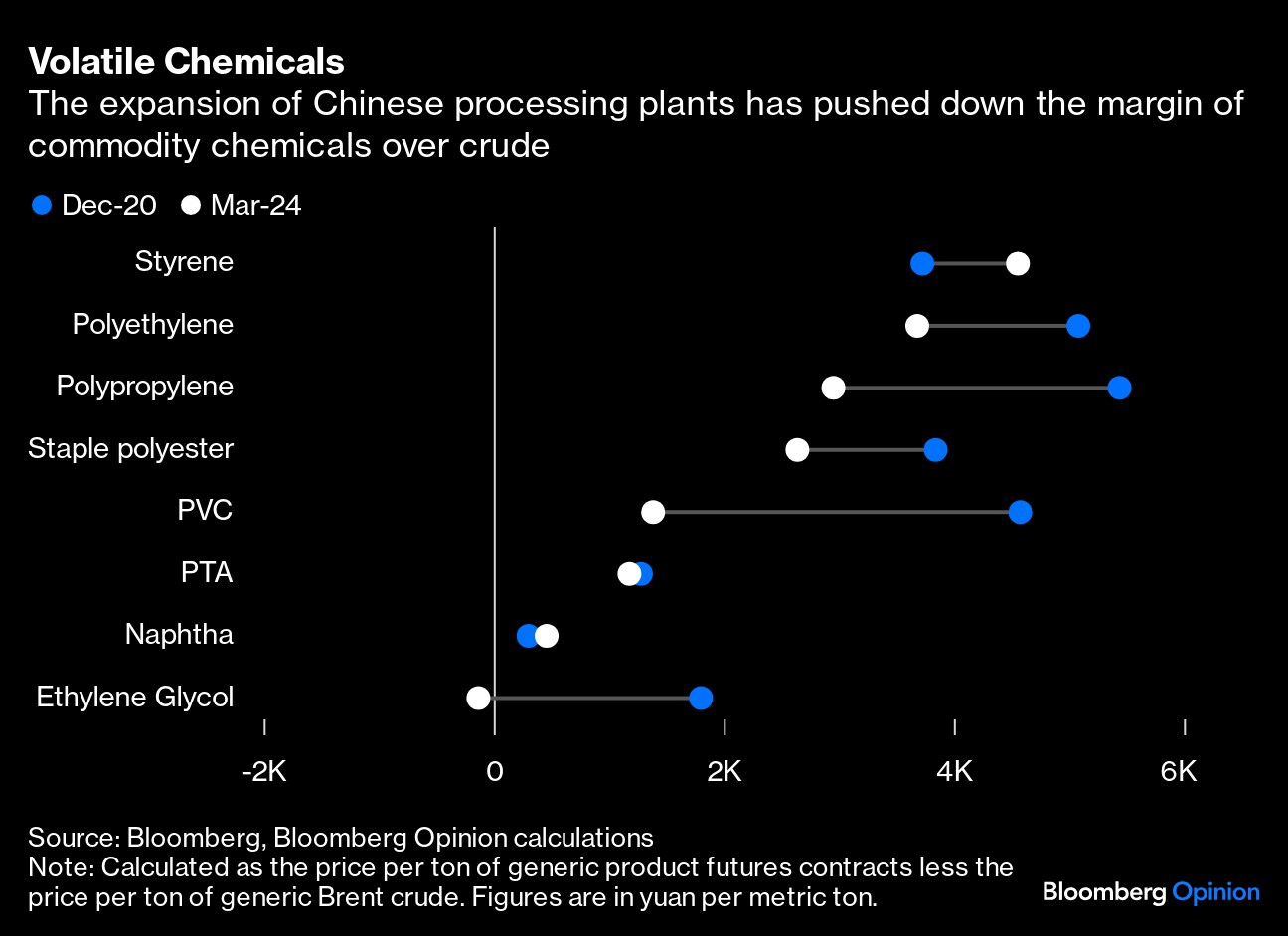

The best way to understand this apparent contradiction is to remember oil consumption in the world's biggest emitter these days isn't so much about GM and Toyota as Shein and Temu — because it's being driven by chemicals, not vehicles. If Chinese oil consumption is growing, it's because the country is aggressively moving its petrochemicals sector onshore, displacing demand that was previously served by imports from Japan, South Korea, the Persian Gulf and Europe.

The climate implications could be significant. Such a move doesn't necessarily increase consumption, and consequent pollution; it may end up doing no more than move the location of processing facilities.

Furthermore, petroleum fuels must be burned to be used, instantly putting emissions into the atmosphere. Petrochemicals, however, tend to keep their carbon locked up in their molecular structures. Though they're anything but CO2-free, an oil industry shifting from fuels to chemical feedstocks is likely to see emissions decline even ahead of a peak in liquid fuels usage.

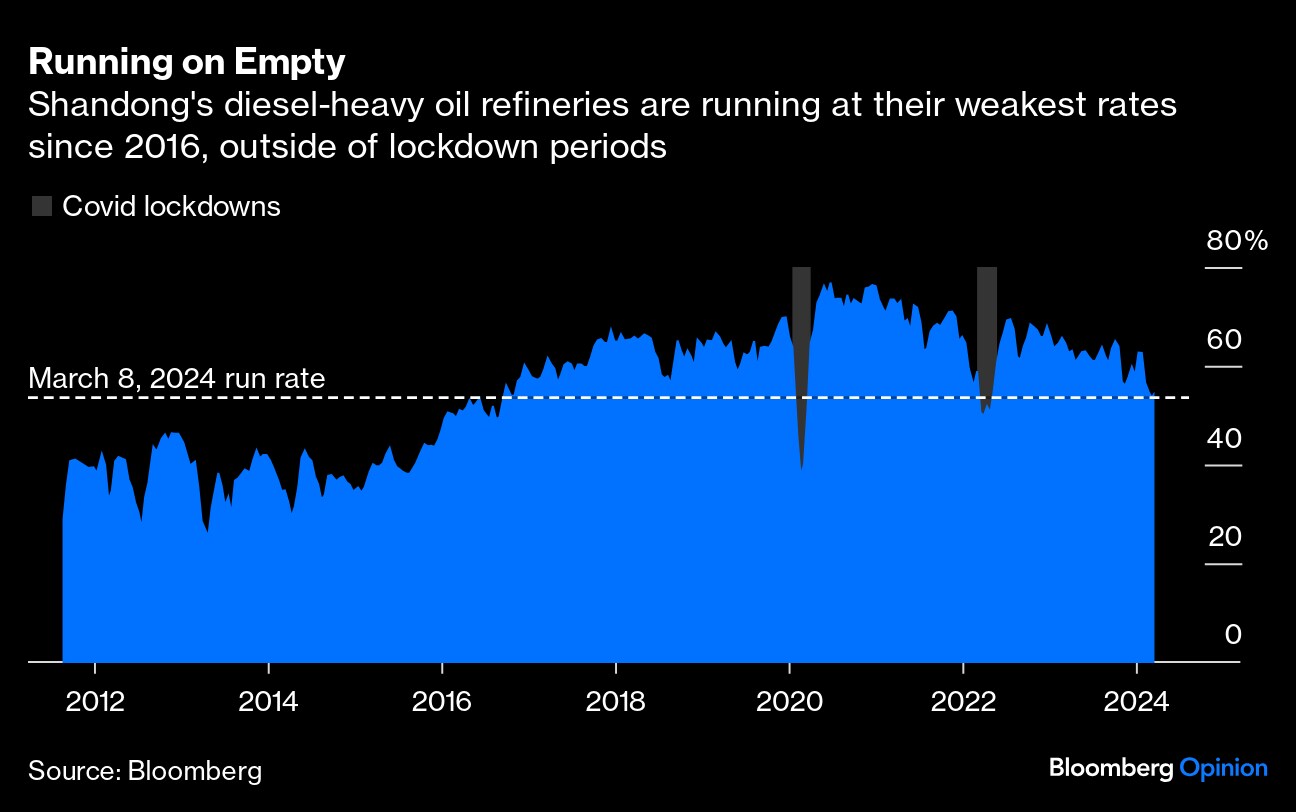

Consider the so-called teapot refineries, a group of privately-owned chemical plants in Shandong province that specialize in producing diesel for trucks, trains and generators. Run rates in recent weeks have been at their slowest pace, outside of pandemic restrictions, since 2016:

That makes no sense in a world where Chinese travel is surging — but it's entirely consistent with what's actually been happening in recent years, where a new breed of private refiners such as Rongsheng Petrochemical Co. and Hengli Petrochemical Co. have been spending billions building plants specializing in chemicals rather than gasoline and diesel.

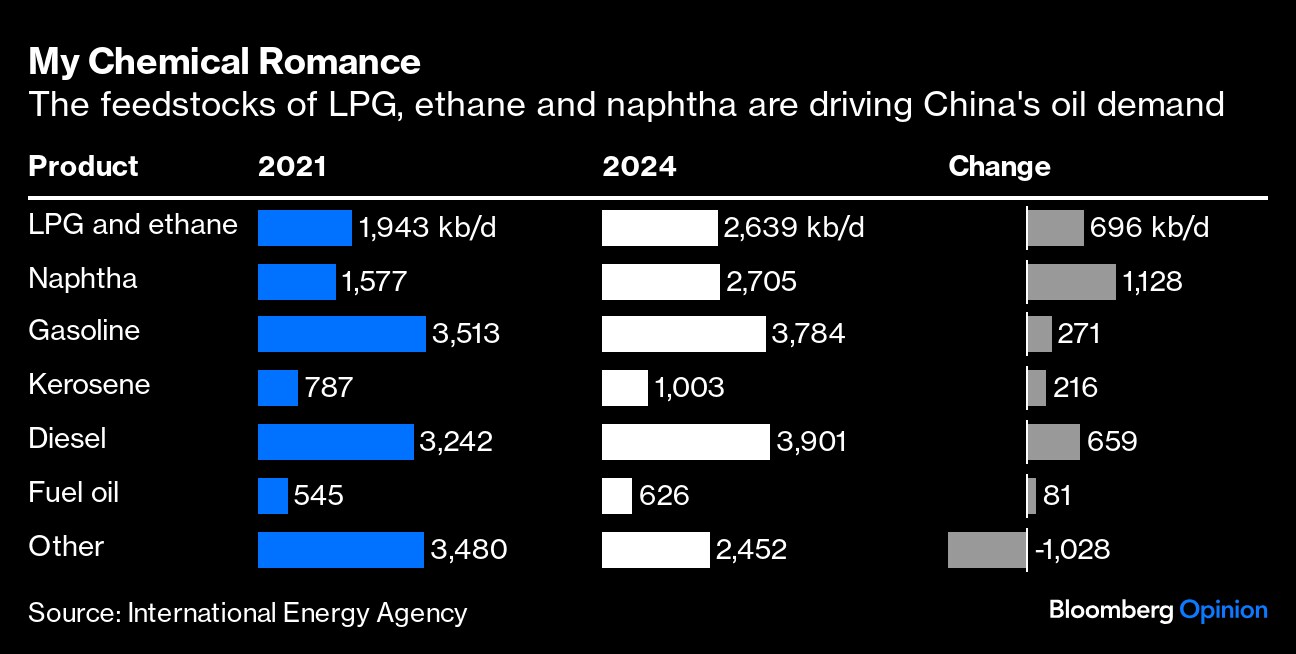

Roughly 90% of China's increased thirst for oil between 2021 and 2024 is coming from the chemical feedstocks of LPG, ethane, and naphtha, according to the International Energy Agency. Gasoline and even jet fuel and kerosene are barely increasing:

Additional Chinese production capacity for the key chemical inputs of ethylene and propylene between 2019 and 2024 will exceed what presently exists in Europe, Japan and South Korea put together, IEA oil market analyst Ciaran Healy noted in a commentary last December. “Global oil demand excluding petrochemical feedstocks remains lower than in 2019 and has grown little since 2017,” he wrote.

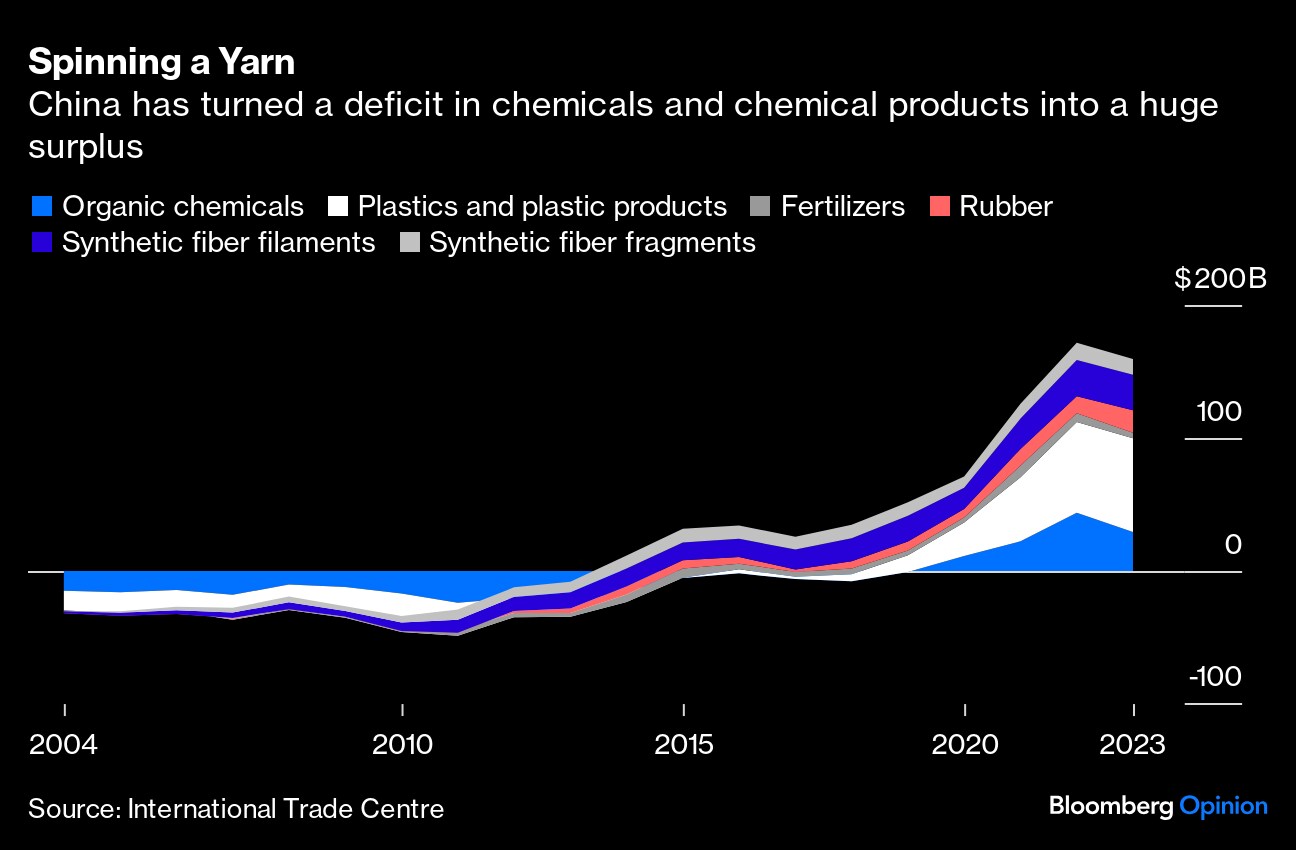

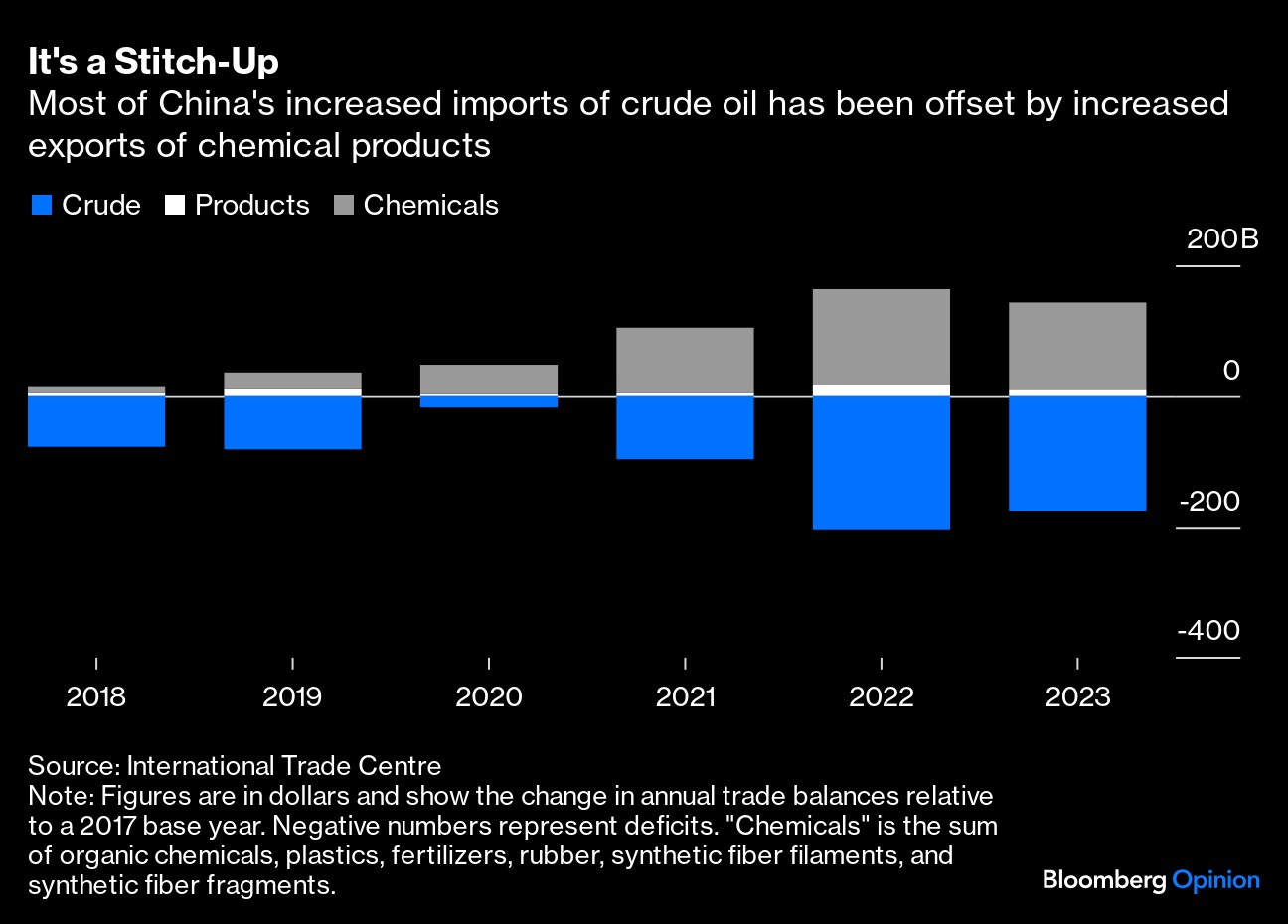

Petrochemicals had historically been an exception to Beijing's general push to be self-sufficient in basic materials, but the new plants being built by Rongsheng, Hengli and even offshore players such as BASF SE are changing that picture. As a result, traditional trade deficits in most downstream oil derivatives are turning into substantial surpluses:

China's output of synthetic fibers alone rose by 21 million metric tons between 2018 and 2023 — enough to spin more than 100 billion T-shirts a year. If you're seeking an explanation for the remarkable persistence of “Chinese oil demand,” you're better off looking at the world's consumption of plastic products and cheap clothing from the likes of Shein Group Ltd. and PDD Holdings Inc.-owned Temu, rather than travel behavior.

A crucial question for the direction of the global climate is how the rest of the world now responds. Executives running petrochemical facilities outside China are facing glutted markets erasing their profit margins. The EU in November imposed anti-dumping duties on Chinese products made from PET, the type of plastic derived from polyethylene that's widely used in bottles.

Indorama Ventures Pcl, the Thai chemicals business that's the biggest producer of PET worldwide, will spin off two of its most profitable units and restructure its business to navigate “fundamental long-term changes in global chemical markets” amid subdued Chinese demand, the company announced earlier this month.

In Europe, competition from the influx of low-cost Chinese products in recent months has been an issue for chemicals producers on a par with the disappearance of cheap Russian gas as feedstock. “We see imports from China coming in, in an order of magnitude like never before,” BASF chairman Martin Brudermüller told an investor call last month.

Right now, plants outside China are still holding on and pumping out products at a loss, in the hope that global consumption of plastics will eventually catch up. There's no guarantee when, or even whether, that happens. Should the global chemicals sector capitulate to the tidal wave of polymers flowing out of China and shut down, 2024's demand surge might look like oil's last gasp, before decline and fall set in.

More From Bloomberg Opinion:

- The Crude Truth Is Oil's Not What It Used To Be: David Fickling

- Shein May Face More Scrutiny Listing in London: Andrea Felsted

- Chinese Are Making a Killing Everywhere But in China: Shuli Ren

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering climate change and energy. Previously, he worked for Bloomberg News, the Wall Street Journal and the Financial Times.

More stories like this are available on bloomberg.com/opinion

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.