More Pain Looms for EM as Lousy Quarter Sputters Toward End

A dark quarter for emerging-market bulls is nearing an end, but things may not be much brighter down the road.

(Bloomberg) -- A dark quarter for emerging-market bulls is nearing an end, and it’s not clear whether things will get much brighter down the road, especially in the near-term.

Currencies, stocks and bonds in developing nations are closing out their worst quarter since 2015 and facing a looming trade war, tightening U.S. monetary policy, elections in Latin America and a weaker global growth outlook. Valuations may look appealing, but this thicket of risks has some investors cautious about plunging back in.

The consensus is that, whether emerging markets are set for a rebound or a deeper sell-off, in the short term the asset class is at the mercy of trade headlines. Goldman Sachs Group Inc., Morgan Stanley and Citigroup Inc. have warned in recent days that more pain lies ahead thanks to the tit-for-tat tariffs between the U.S. and China. And even those on the bullish side, like UBS Global Wealth Management -- which forecasts a double-digit rally in stocks -- are waiting for trade rancor to die down before fully jumping in.

“From a valuation standpoint, there are attractive values. But on a tactical basis, we think there may be more pain in the next few weeks,” said Alessio de Longis, a portfolio manager at OppenheimerFunds Inc. in New York, whose Global Multi-Asset Income Fund has outperformed 89 percent of peers in the past month.

He also pointed out that the concern over market-unfriendly candidates winning elections in Mexico and Brazil as well as typical risk-aversion during summer in the Northern Hemisphere could put pressure on emerging-market currencies in the coming months.

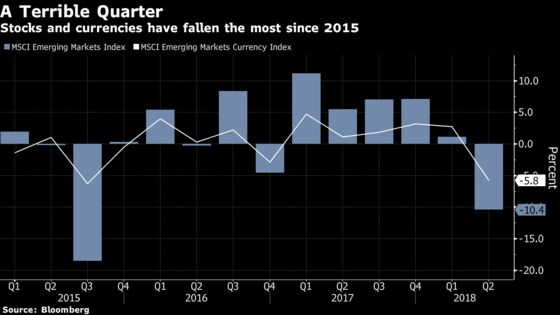

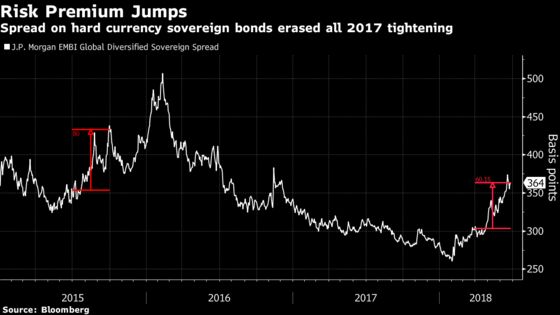

What looked like a moderate downturn earlier this year turned into a full-fledged plunge in the second quarter. The MSCI benchmark index for stocks has fallen about 11 percent, currencies have dropped almost 6 percent and the spread on hard-currency sovereign bonds has widened by 66 basis points. These are the worst quarterly results since September 2015, when developing-nation assets were in free-fall following a meltdown in Chinese stocks and an unexpected devaluation of the yuan.

The stark result stands in contrast to the common refrain about the relative health of emerging markets. Certainly few investors predicted a repeat of the rally in 2017 but many cited maturing financial markets and reformed political systems as reasons to remain optimistic about a sector that now accounts for about 70 percent of global gross domestic product. In February, Jeremy Grantham, the 79-year-old investor known for his bearish views, said he advised his own kids to invest more than half their retirement money in the asset class.

"If an investor was lucky or smart enough to have had all the risky and high-yield bonds in that trend, that trend is now exhausted," said Michael Roche, a strategist at Seaport Global Holdings LLC in New York. “I have been calling for and continue to call for caution. Portfolio managers should turn to safer holdings from risky holdings."

Currencies vs. Bonds

Local-currency bonds from emerging markets were also burned, as their returns to foreign investors are automatically squeezed if the dollar strengthens. And they haven’t recovered as the greenback has continued rising. A Barclays’ index for local-currency bonds from developing nations has fallen 6 percent this quarter, more than erasing the 3 percent gain of the first quarter.

Outflows have hit almost all markets and were recently a highlight in South Africa as foreign investors rushed to sell local bonds, draining their holdings to the lowest level in more than a year, as the rand slumped and the country seemed vulnerable to a more sour external backdrop.

The currency depreciation that hammered bonds triggered central bank responses in many emerging markets. Argentina increased its benchmark rate 675 basis points to 40 percent amid the peso collapse. Turkey also raised rates, defying President Recep Tayyip Erdogan’s bid for a looser policy. India, Indonesia and Philippines also tightened their policies and Brazil stopped an easing cycle earlier than expected while it heavily intervened in the currency market to fight the real’s free fall.

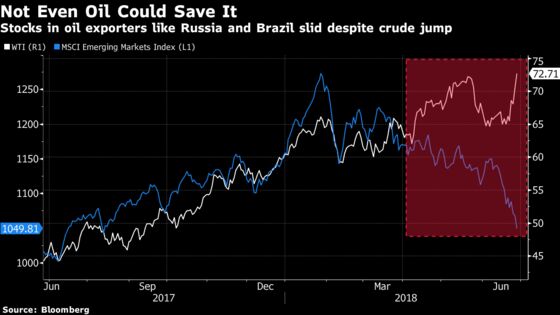

“EM central banks are responding in an orthodox way,” said Timothy Ash, an emerging-market sovereign specialist at Bluebay Asset Management in London. However, “if concerns over a trade war hit global growth and then this feeds through into commodities, then we might have a proper EM bear market.”

Stocks and China

China, the world’s second-biggest stock market, entered bear territory as the yuan slumped, and even investors’ favorite stocks got hammered. The FTSE China A50 gauge of the largest mainland companies by market value closed Wednesday at its lowest level since last July, while Chinese stocks in Hong Kong sank 21 percent from their January peak.

That sell-off was another source of pressure on emerging-market stocks. The combined market value of 24 emerging markets tracked by MSCI has fallen by more than $2 trillion this year. Morgan Stanley strategists lowered their 12-month target for the MSCI emerging-markets index to 1,000 from 1,160 and cut their equity allocation to add cash. That benchmark fell four a fourth day to 1,043.90 as of 11:14 a.m. in New York.

Investors in exchange-traded funds, who earned 85 percent returns during the two-year rally in emerging-market stocks, also turned pessimistic. Withdrawals from the iShares MSCI Emerging Markets ETF exceeded $5 trillion in the second quarter, rivaling levels seen during the euro-area debt crisis and the winding down of Federal Reserve stimulus in 2014.

As cash investors run for the exits, short sellers are moving in for the kill. They have added more than $1.8 trillion of bets in the last three weeks, wagering that emerging-market stocks will keep dropping. That’s taken the short positions on the ETF to their highest level since September.

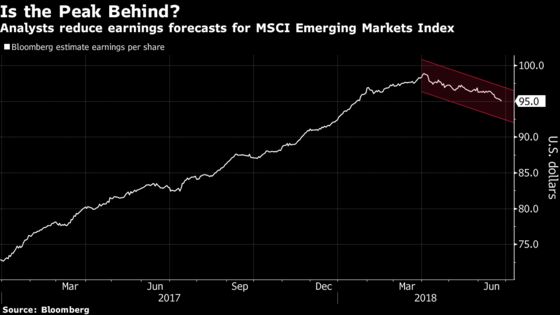

Analysts are cutting earnings estimates for the first time in six quarters. While emerging-market growth remains intact, there’s greater concern that the threatened U.S.-China tariffs will reduce global demand and impair export-dependent economies. Estimated earnings per share for the MSCI EM index fell for a 10th consecutive day on Wednesday.

Opportunity Knocks

Some investors, however, see opportunity amid the wreckage. Greg Lesko, a money manager at Deltec Asset Management in New York, says that while there are “plenty of hurdles” for emerging markets, the recent sell-off has opened buying opportunities because, in the longer run, economic fundamentals remain strong.

“With a forward price-to-earnings ratio somewhere just over 11, all EM looks cheap," he said. “The challenge and risks are mostly political."

To contact the reporters on this story: Aline Oyamada in Sao Paulo at aoyamada3@bloomberg.net;Giulia Morpurgo in New York at gmorpurgo1@bloomberg.net;Srinivasan Sivabalan in London at ssivabalan@bloomberg.net

To contact the editors responsible for this story: Rita Nazareth at rnazareth@bloomberg.net, ;Jeremy Herron at jherron8@bloomberg.net, Andrew Dunn

©2018 Bloomberg L.P.