(Bloomberg Opinion) -- The best thing that might be said about Tesla Inc.'s first-quarter sales numbers released Tuesday is that the company won back the crown of biggest battery electric vehicle maker in the world. The more fanatical bulls might cling to that. Everyone else can save the high-fives.

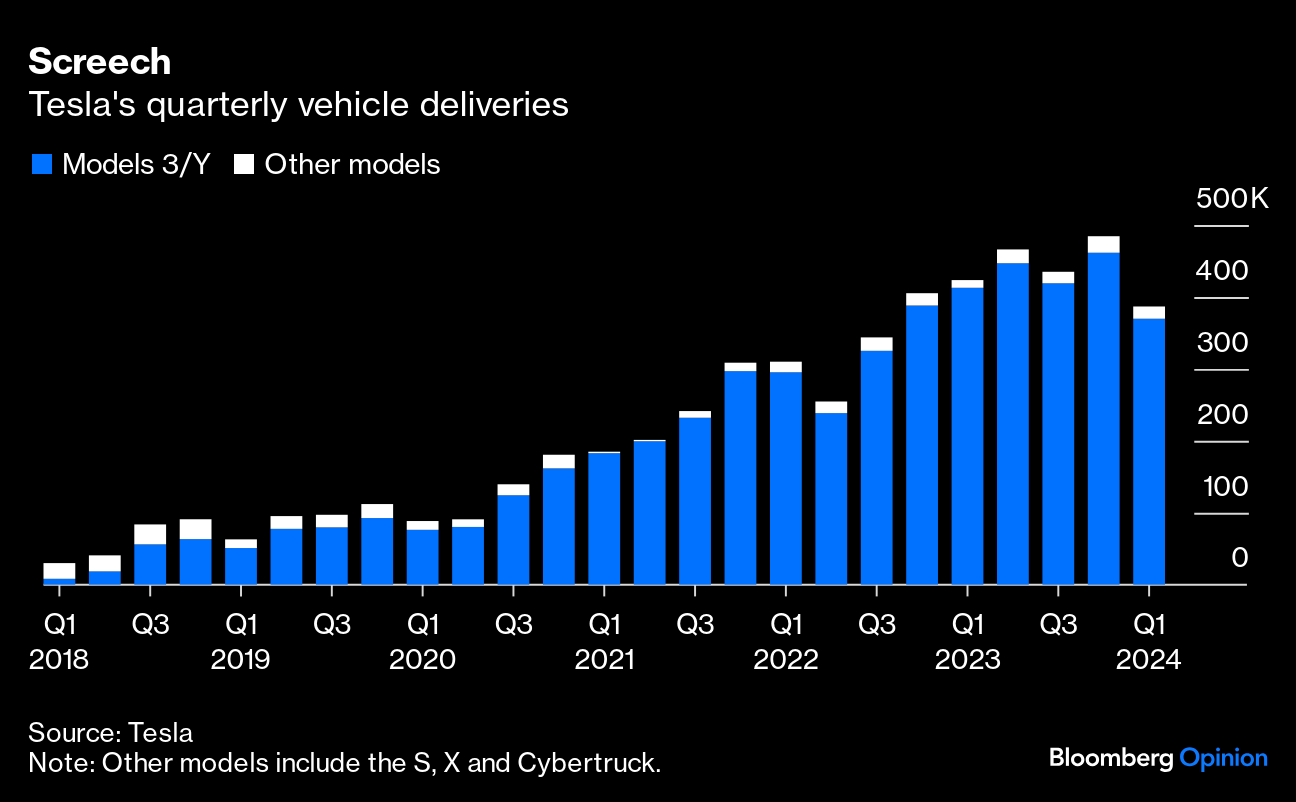

Heading into Tuesday, the consensus estimate for Tesla's vehicle deliveries had been dropping at a brisk rate. A year ago, analysts expected Tesla to sell about 530,000 vehicles in the quarter just ended. By the start of the year, they had tweaked that down to half a million, and had dropped it since to just under 450,000. Tesla missed even that by 14%, reporting just under 387,000. True, that beat main rival BYD Co. Ltd., which surpassed Tesla's sales in the fourth quarter of 2023, but only because BYD's sales of battery electric vehicles fell by even more.

This is the first year-over-year decline in Tesla's vehicle deliveries since the pandemic.

Weakness was broad-based. Despite the addition of the Cybertruck at the end of 2023, sales of Tesla's higher-price models came in at about 17,000, within the typical range of 15,000 to 20,000. Sales of the mainstay 3 and Y models were also weak, hitting their lowest level since the summer of 2022.

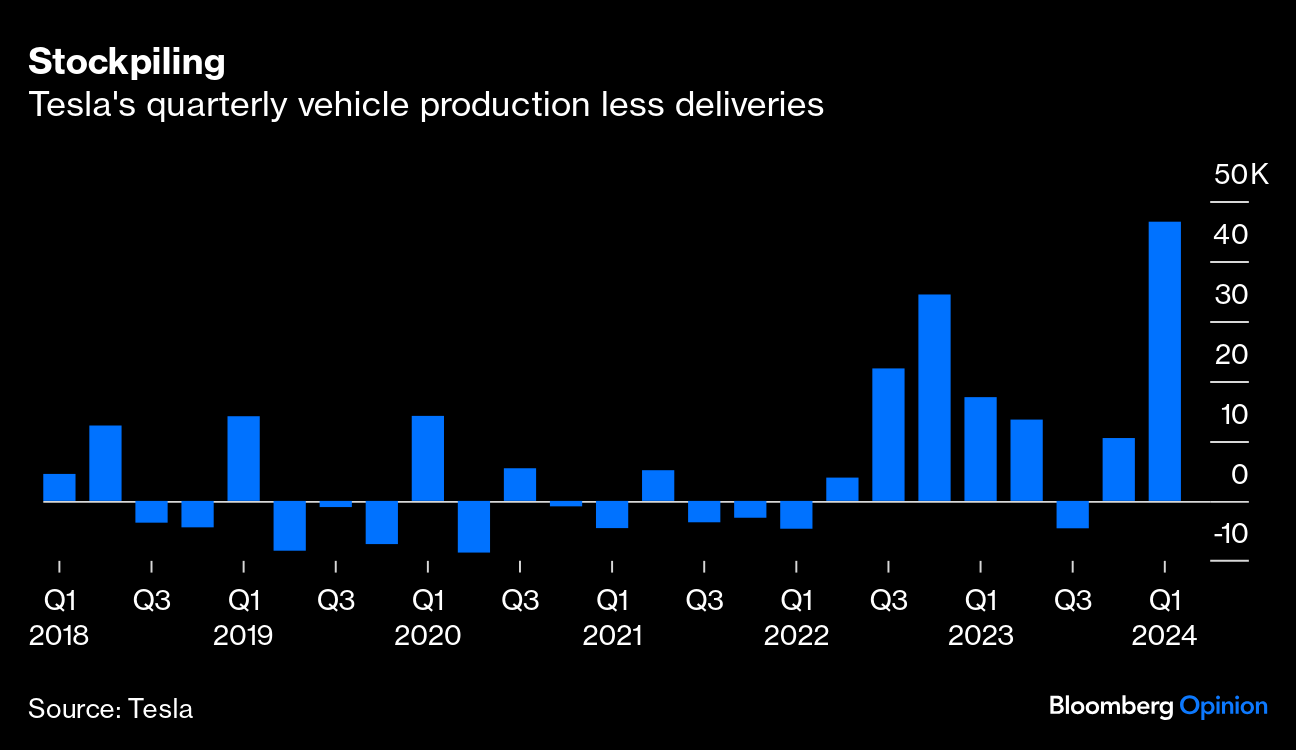

Tesla blamed several factors related to production and logistics, including its refresh of the Model 3, the blackout that hit its factory near Berlin and shipping disruptions in the Middle East. Yet production still outpaced deliveries by the widest margin yet, at more than 46,000 vehicles. Tesla has now produced more vehicles than it sold in seven of the past eight quarters.

The immediate implication is that with Tesla having missed even the lowest estimate in Bloomberg's consensus table, first-quarter financial estimates must be torn up. The emerging narrative since the start of 2023 has been a series of price cuts that failed to spark a rebound in sales, crushing margins. These figures point to a reckoning when financial results are released in three weeks. Given the investment in the Cybertruck, its implied slow start — or, perhaps, weakness in sales of the Models S and X — will weigh on margins. Moreover, the big buildup in finished inventory, a working capital sink, presents a formidable headwind to cash flow.

Looking ahead to the year as a whole, analysts were forecasting Tesla to deliver just over two million vehicles in 2024. That implies growth of just 11%. After these figures, however, Tesla would need to sell an average of about 543,000 in each of the next three quarters to hit even that. That would be a marked turnaround not only from the quarter just gone, but Tesla's best quarter to date, the prior one, when it delivered about 485,000 vehicles. Besides first-quarter estimates, earnings expectations for the year require big revisions.

It perhaps goes without saying that it is just odd that Tesla, a member of the S&P 500 sporting a market cap of over half a trillion dollars, didn't bother to issue any sort of warning ahead of missing estimates so widely. Then again, we got a warning of sorts last week when an internal email from Chief Executive Elon Musk leaked. In it, he mandated that all buyers in the US would have to be given a short demonstration of Tesla's “full-self driving,” or FSD, driver assistance technology before getting their vehicle. Later that day, he also announced, on X, free one-month trials of FSD for those drivers who hadn't taken it.

Musk has any number of reasons to push full self-driving; at least 12,000 of them. That's the price, in dollars, you pay for the option and, assuming software-like margins of about 90%, it transforms the profits, given that Tesla's average gross margin per vehicle sold last year was a bit less than $9,000. In addition, despite FSD not actually fully self-driving the vehicle — Musk referred to it as “(supervised) FSD” in his email, and those parentheses are doing yeoman's work — the concept of robotaxis is critical to Tesla's inflated valuation, so it helps to keep the dream alive.

Musk also noted in his email that the demonstrations would likely slow down sales, which at least makes for a nice line when folks inevitably ask about the drop in sales on the eventual earnings call. Given how dreadful earnings are likely to be, and Tesla's stock being the worst performer in the S&P 500 so far this year, a share buyback remains a distinct possibility. Yet resorting to that would also serve to emphasize the main problem: the glaring mismatch between soaring expectations embedded in Tesla's valuation and the hard reality of its reported numbers.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy. A former banker, he edited the Wall Street Journal's Heard on the Street column and wrote the Financial Times's Lex column.

More stories like this are available on bloomberg.com/opinion

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.