Demonetisation was supposed to move consumers away from cash and towards digital payments, including credit and debit cards. Many believe that it didn't play out that way.

Currency in circulation as a percentage of GDP, a measure of the cash in the economy, has almost moved back towards pre-demonetisation levels. As of March 2019, currency in circulation is expected to be 11.4 percent of GDP, only marginally lower than the 11.9 percent of GDP ahead of demonetisation, showed a HSBC report dated Feb. 11.

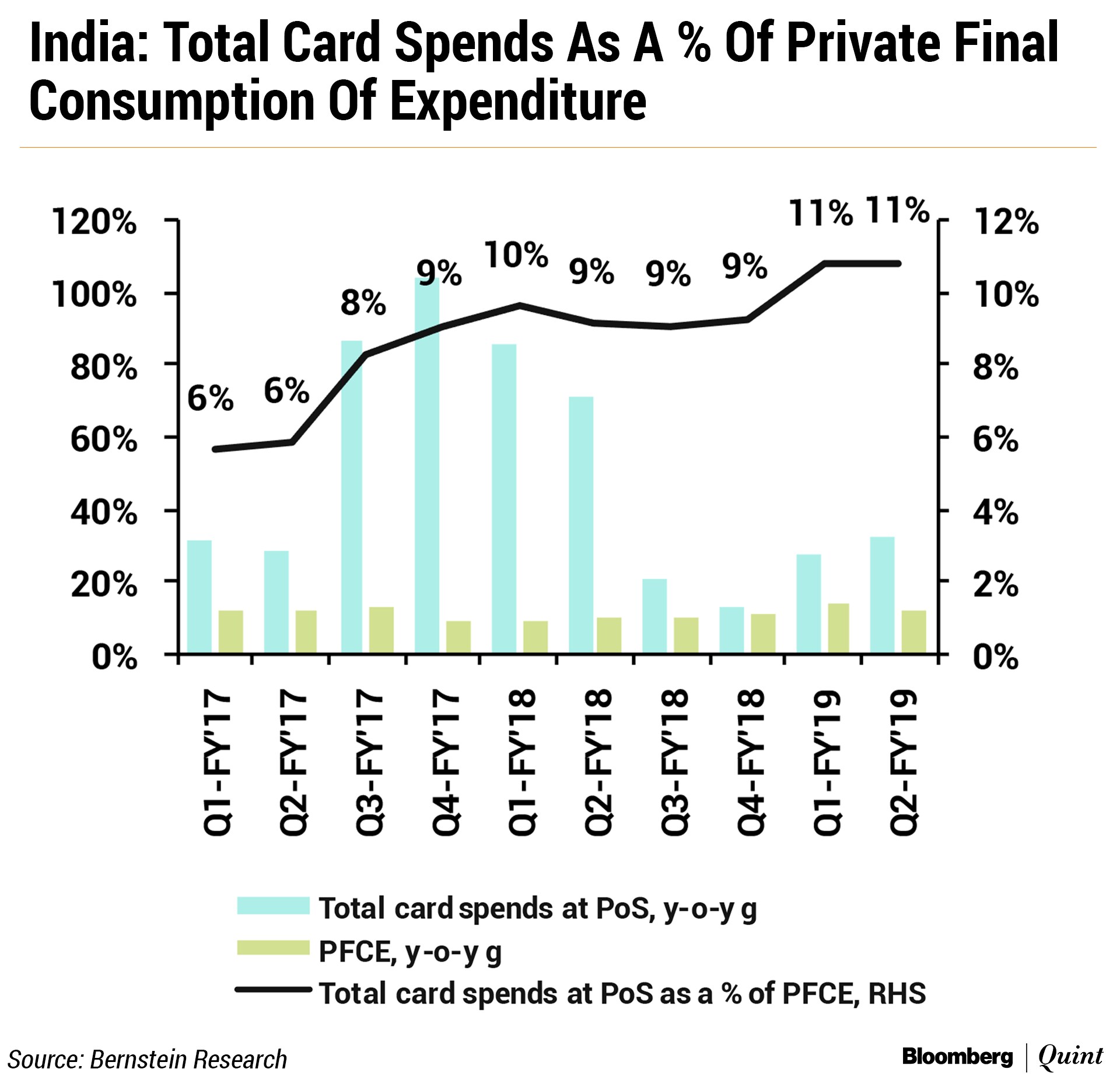

While cash usage in the broader economy may not have fallen sharply, a research note by Bernstein Research shows that a larger proportion of consumption spending is happening via cards.

Total card spends as a percentage of private consumption expenditure has nearly doubled from 6 percent in the quarter ended September 2016 to 11 percent in the quarter ended September 2018 quarter, said a Bernstein research note released on Monday.

To assess card spends, the research house used both credit and debit card payments at point-of-sale terminals. Private consumption expenditure is a component of GDP measured from the expenditure side.

Since demonetization in Nov. 16, quarterly card spends have almost doubled. Card spends growth continues to significantly outpace the growth in private final consumption expenditure. As a result, the share of card spends in PFCE has been steadily moving up and nearly doubled from 6 percent in the pre-demonetization era (Q2FY17) to 11 percent.Gautam Chhugani, Analyst, Sanford C. Bernstein & Co.

Credit card spends, on a trailing 12-month basis till November 2018, grew at 32 percent year-on-year rate, compared to a 16 percent growth rate for debit card spends. Growth in credit card spends, in particular, is being driven by strong rewards and loyalty incentives by banks and partnerships with online merchants, the research note stated.

“For both credit card and debit card, growth in spends is being driven by volume growth rather than ticket size growth indicating rise in user penetration and usage,” Chhugani and fellow analysts Gaurav Jangale and Monika Agarwal wrote.

Spends across India's indigenous RuPay cards have also been rising, albeit on a smaller base.

Use of RuPay at PoS terminals rose 36 percent year-on-year on a twelve month trailing basis till November 2018. The jump in usage of RuPay cards on ecommerce websites was higher at 114 percent. “Increasing e-commerce penetration combined with a low base has led to more than doubling of RuPay card spends in e-commerce,” said the research.

After the UPI's success and the exponential growth in mobile banking, spending via RuPay and UPI together accounted for nearly 20 percent share in value and 28 percent in volume during November 2018, the report added.

As card usage has picked up and card acceptance infrastructure via PoS has grown, the ATM network has stagnated for more than two years and shrinking slightly.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.