In December 2021, SEBI issued a direction banning futures in four agri-commodities for a period of one year. In August and October 2021, SEBI had banned futures in three other agricultural commodities. These seven commodities constituted more than 70% of the traded volumes in the Indian agri-commodities futures market. In an article written soon thereafter, we had argued that the ban was bad economics and bad law. We demonstrated that the ban had no impact on the prices in the spot market of two of these commodities, namely Chana and RM mustard seeds, which were banned in August and October; it imposed disproportionate restrictions on the fundamental right to trade conferred under the Indian Constitution; and it was inconsistent with SEBI's market development mandate.

Three months later, we have the benefit of time to assess whether the ban fulfilled its avowed purpose of driving down or stabilising the price of the remaining banned commodities in the spot market. In this article, we demonstrate that the ban has not served its purpose and warrants a review.

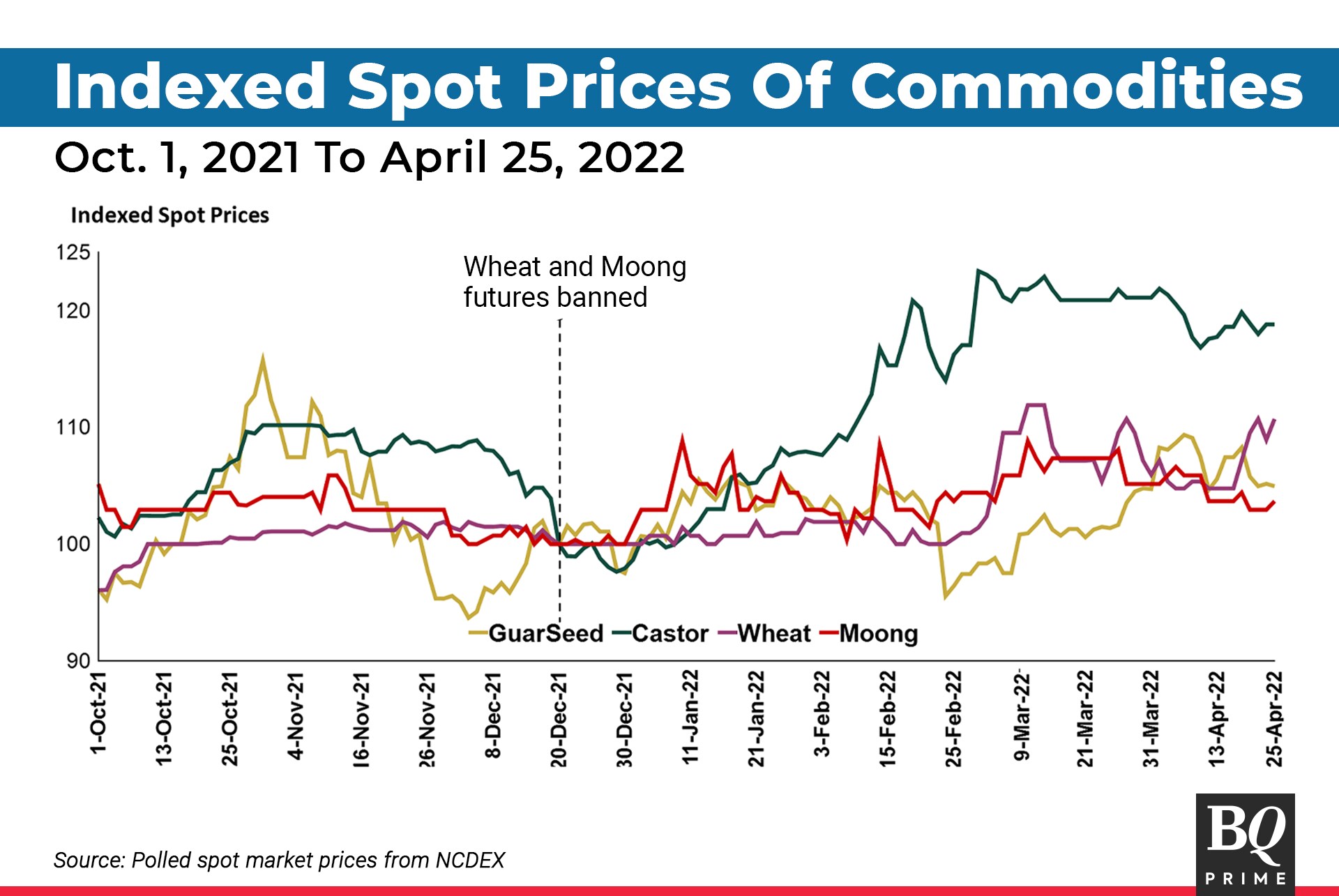

What Happened To Spot Prices?

We examine the spot prices of the two commodities, namely Wheat and Moong, for which futures were banned in December 2021. To contrast them with commodities that were not banned, we also look at two such commodities – Castor and Guar Seed. To be sure, Castor and Guar Seed futures contracts are significantly more liquid than the banned commodities in the agri-futures market. However, they provide a useful counterfactual to understand the general price trends in the spot market.

The chart below shows the indexed spot prices of these four commodities, where the price on Dec. 20, 2021, is taken as 100. We trace the price of these commodities for a period of two months prior (From Oct. 1, 2021) and four months after the imposition of the ban. The chart shows that the price of wheat at the time of the ban was relatively stable and continued to remain stable thereafter until February 2022.

The ban appears to have had no impact on the spot price of wheat. The price of Moong similarly remained stable until December and then, in fact, increased from January.

Overall, the graph suggests that the spot prices of each of the banned and permitted commodities followed a random walk, and were responding to underlying demand and supply conditions.

There are two reasons for this.

First, since the underlying commodities are agricultural, the information about cropping area, production and harvest levels, etc. are a more important determinant of spot prices, which react as such information is released over time. For some commodities that are globally traded (such as wheat), global events that can impact global demand-supply can influence domestic spot prices. For example, this is evident in the price of wheat which shows a secular rise after the third week of February in the wake of the Russian invasion of Ukraine.

Second, as we showed in our earlier article, futures in wheat and moong are not very liquid, which further reduces the possibility of the ban having any impact on the spot market. If anything, a long-term ban of this nature obliviates the possibility of developing this segment of the market altogether.

Harmful For Farmers

In the absence of liquidity in these two commodities, the ban on Moong and Wheat futures likely does not have as deleterious an impact on price formation and dissemination as it has for the other banned commodities, namely soybean, refined soy oil, and chana, which are more liquid. However, the ban in the futures market nevertheless deprives farmers in more ways than one.

First, it deprives them of the information that they could have used to benchmark their prices in the spot market.

Second, it deprives farmers of the opportunity to lock in higher prices for their produce.

For instance, demonstrated through the chart, theoretically speaking, farmers, farmer producer organisations, and wholesale traders could have locked in the price of Moong when it was at its peak in January 2022. Similarly, in 2022, wheat procurement in India has been the lowest in fifteen years. This is partly because farmers have been able to sell their wheat in the open market at a price higher than the MSP, and take advantage of the nearly 100% increase in the global price of wheat over last year.

A combine deposits harvested wheat in a tractor trolley, on the outskirts of Ahmedabad, on March 16, 2022. (Photograph: REUTERS/Amit Dave)

Implications For Regulatory Governance

The agri-futures ban story reinforces two key norms about regulatory governance.

First, the failure of the ban fortifies the case for conducting periodic assessments of bans and prohibitions in India, especially those that are imposed overnight, without public consultation or a statement explaining the reasons, costs, benefits, and the expected outcomes of the intervention.

A ban on futures markets in agricultural commodities designed to last for as long as a year in what is likely to be the most volatile period for commodity prices and overall food inflation, is expensive and brash.

A systematic review of the ban would entail evaluating the impact of the action objectively, including assessing whether the objectives of the regulatory intervention are met and the costs impact (including collateral costs). In the absence of a mechanism to conduct such a review, ineffective and even harmful regulatory actions will continue unabated for a long period.

Second, the objective of establishing an independent regulator insulated from an elected executive is to secure policy stability. This is the core idea of credible commitment where the state cedes its sovereign monopoly to govern a segment of the economy to signal its commitment to regulate in public interest. Overnight unpredictable interventions of this nature effectively suggests that the state has reneged on this commitment.

Finally, as has been argued by many commentators before us, the development of a derivatives market in agricultural commodities should be our national priority given the significance of agriculture in our economy and fiscal balance sheet. Such a development mandate is hardwired in SEBI's governing law making it incumbent upon the regulator to resist the impulse to ban and prohibit entire segments of a nascent market.

Harsh Vardhan is a management consultant based in Mumbai. He is also a public interest director on the board of National Commodity Clearing Ltd. These are his personal views. Bhargavi Zaveri-Shah is a doctoral candidate at the National University of Singapore.

The views expressed here are those of the authors, and do not necessarily represent the views of BQ Prime or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.