Financial year 2012-13 was a tough year for India.

Growth in the economy had fallen to below 5 percent – a decade low. Delays in government approvals had stalled a number of large projects, hitting cash flows of companies that were implementing them. Inflation was soaring and consumer confidence was low.

The country's lenders hadn't seen this coming. They had been growing their loan books at a compounded annual growth rate (CAGR) of almost 20 percent over the past five years. As the economy slowed and loans started to show signs of stress, banks simply threw them into the corporate debt restructuring cell which allowed them to recast the debt on easy terms with little additional provisioning.

In was in the midst of this environment, in August 2012, that Credit Suisse released its first ‘House of Debt' report authored by Ashish Gupta and Prashant Kumar.

Over last five years, Indian banks havewitnessed strong (20 percent CAGR) loan growth. However, this has increasinglybeen driven by select few corporate groups; aggregate debt of these tengroups has jumped 5 times in the past five years and now equates to 13 percent ofbank loans and 98 percent of the banking system's networth.Credit Suisse House of Debt Report - August 2012

In the four years since the release of that report, much has happened. A new government has been elected; growth has revived to above 7 percent; forbearance on restructured loans has ended. Most importantly, the Reserve Bank of India has forced banks to recognise the hidden stress on their balancesheets, pushing a number of the firms identified in the House of Debt report into the stressed loan category. These companies are now in the process of deleveraging through asset sales and more.

Gupta, now head of research at Credit Suisse, took stock of the deleveraging process in a September 19 report and noted that nearly 39 percent of debt is still in the hands of companies which don't even earn enough to cover their interest payments. While companies in the commodity segment have seen some improvement due to the bottoming out of the cycle, others in sectors like infrastructure and power continue to struggle. As a result, 53 percent of debt is still with companies that have a debt-EBITDA (earnings before interest, tax, depreciation and amortisation) of more than 12 times.

.jpg)

In an interview with BloombergQuint, Gupta said the pace of deleveraging is slower than they would have expected three to six months back.

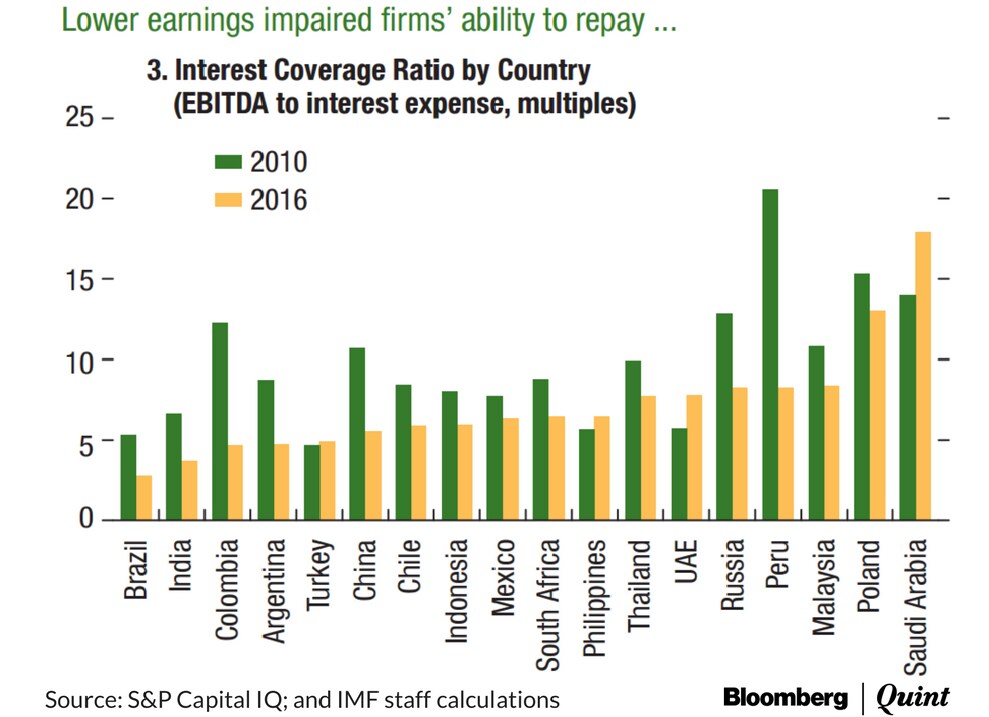

Corporate balancesheets which were eight feet under water may now be four feet under water but they are still under water, he said. While the aggregate interest coverage ratio of Indian firms has increased, the improvement is not well distributed. The interest coverage ratio is an indicator which reflects a company's ability to cover its debt repayments.

“In 2014, the number companies with interest coverage of less than 1 used to be about 35 percent. It moved to a peak of 42-43 percent in the September-December 2015 quarters which is when the commodity cycle was at the bottom. Since then it has come back and we are at now at 38-39 percent,” said Gupta.

Credit Suisse's analysis captures what two separate data points released over the past fortnight tell us about corporate credit quality in India.

In its semi-annual review of corporate credit quality, rating agency CRISIL said that the debt-weighted credit ratio for firms rated by it rose to two for the first half of the fiscal compared to 0.2 in the second half of fiscal 2016. The ratio, which reflects the amount of debt on the books of companies downgrades compared to that on the books of companies upgraded, rose above one for the first time in five years, said the rating agency. The ratio of the number of companies upgraded to those downgraded also rose to 1.2 times compared to 0.8 tomes in the second half of last year.

While CRISIL's numbers pointed to a clear improvement, a reality check came through in the IMF's Financial Stability Report released on October 5. That report showed that the interest coverage ratio of Indian firms is the second lowest among emerging economies after Brazil.

The simple point - corporate balancesheets in India have a long process of repair to undergo before they can be called healthy again.

The House Of Debt-10

The ten groups that the House of Debt had identified back in 2012 as being significantly over-leveraged included Lanco Group, Jaypee Group, GMR Group, Videocon Group, GVK Group, Essar Group, Adani Group, Reliance Group, JSW Group and Vedanta Group.

The core businesses of these groups lay either in the commodity segment or in the infrastructure segment. Given this similarity, the fortunes of these groups followed a common path between the 2012-2015 period. Over the past six months, though, there has been a divergence because of the relative stability in commodity prices. This has meant that groups that had a heavier reliance on commodities have seen an improvement.

While the latest report from Credit Suisse did not focus on individual groups, it highlighted that leveraged metal companies have seen an improvement.

Over the past two quarters, with the imposition of minimum import price, performance of metal companieshas improved. As a result of this, the share of metal companies within interest coverage (IC) <1 has comedown sharply from 36 percent as of December 2015 to 26 percent in March 2016 and 18 percent in June 2016. Thedecline in metals is largely on account of Tata Steel exiting the list in this quarter, followingthe exit of Vedanta, Hindalco and JSW Steel in the fourth quarter of fiscal 2016.Credit Suisse India Corporate Health Tracker

Meantime, groups with larger exposure to segments like power are still struggling. Low plant load factors, stranded gas-based capacities, unviable power purchase agreements and falling merchant power rates are factors that continue to hurt groups involved in the power sector.

Asset sales which had picked up in the first six months of the fiscal also appear to have slowed once again.

In a May 15 report, Kotak Institutional Equities had noted that Rs 41,000 crore in stressed asset sales were closed in the first five months of 2016, taking the total tally of such sales since 2013 to Rs 1 lakh crore. In recent months, while a few groups like the Jaypee group have continued to sell assets, the pace has slowed.

Asset sales needs to pick up again, said Gupta while adding that asset sales alone may not help but they need to be part of the broader solution for corporate debt.

Where Does This Leave Banks?

The slow process of repair of corporate balancesheets means that the worst may not be over for the country's lenders.

Stressed assets, which include both restructured and bad loans, are currently at about 12 percent of total loans. Credit Suisse estimates that there is still some under-recognition of stress and expects total stressed assets to peak at about 16 percent of total loans. This projection is consistent with other indicators across the banking sector. Data accessed by BloombergQuint through a Right To Information query showed that Rs 1.89 lakh crore in loans were categorised as SMA-2 account.

SMA-2 or special mention accounts category-2 are those where repayments are overdue by more than 60 days.

Gross non-performing assets (NPAs) of Indian lenders stood at Rs 6.3 lakh crore as of the end of the September 2016 quarter and a large amount of SMA-2 accounts suggests that NPAs could rise further.

Within the restructured accounts category, too, slippages remain high. According to Credit Suisse, 43 percent of restructured accounts have now turned bad.

.jpg)

Two things could help relieve the pressure for banks – debt structuring schemes announced by the Reserve Bank of India and the interest shown by global stressed asset investors in the Indian market.

According to Gupta, the Scheme for Sustainable Structuring of Stressed Assets (S4A) could prove to be a useful tool. The scheme allows banks to divide a company's debt into a sustainable part and an unsustainable part. The latter is converted into equity-linked long-term instruments while the former is serviced with existing cash flows.

“Some of the schemes that are available today are very pragmatic. Particularly the S4A scheme because it allows banks to cut the debt into two parts – the sustainable part and the unsustainable part. It is needed to revive at least some of the assets,” said Gupta

The scheme has not been used in any large cases yet but bankers are expecting the RBI to rework some of the provisions of the scheme to make it more usable. The regulator will release those revised guidelines by the end of October, it said in its monetary policy review last week.

The interest from global stressed asset investors could also help, said Gupta. Over Rs 30,000 crore in domestic and global capital is chasing stressed assets in India through a series of tie-ups announced in the last few months. While deals have been slow to close, Gupta sees this as a possible relief for banks if they agree to take the requisite haircuts.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.