The worst of the bad loan problem plaguing Indian banks may not be over just yet.

The Reserve Bank of India (RBI), in its Financial Stability Review (FSR) released on Thursday, has cautioned that gross non performing assets (NPAs) for the banking system could rise further to 9.8 percent by March 2017 from 9.1 percent in September. This ratio, under the baseline scenario of economic growth, could rise 10.1 percent by March 2018.

If macroeconomic conditions deteriorate further, the bad loan ratio may even increase beyond those levels, said the central bank.

The RBI, in its December monetary policy review, had reduced its growth forecast for the year to 7.1 percent from the earlier estimate of 7.6 percent. Private forecasters expect growth to fall below those levels due to the impact of the government's decision to withdraw notes of Rs 500 and Rs 1000. The RBI, however, continues to see that as a temporary disruption to economic growth.

The withdrawal of specified bank notes will impart farreaching changes going forward. It is expected to significantly transform the domesticeconomy in due course in terms of greater intermediation, efficiency gains,accountability and transparency through increasing adoption of digital modes ofpayments, notwithstanding the short-term disruptions in certain segments of theeconomy and public hardship.Urjit Patel, Governor, Reserve Bank of India (Foreword To Financial Stability Report)

Public Sector Banks To See Higher Bad Loans

The central bank expects public sector banks to continue to register the highest bad loan ratio. Under its baseline projection, it expects public sector banks' bad loans to rise to 12.5 percent in March 2017, and then to 12.9 percent a year later, from 11.8 percent at the end of September 2016.

For the banking sector as a whole, gross NPAs rose to 9.1 percent at the end of September from 7.8 percent at the end of the last financial year. Total stressed assets in the banking sector, which also include standard restructured accounts, have risen to 12.3 percent from 11.5 percent over the six months ending September, the RBI said.

I think we are in sync with what the RBI is saying on asset quality. We also expect the asset quality to deteriorate, but slower than what we've seen so far. But what is more important than the headline number is that the impact on credit cost will remain high.Abhishek Bhattacharya, Associate Director, India Ratings & Research

The Reserve Bank of India has also noted that the current capital position of Indian banks may be insufficient to support higher credit growth as they will need to divert resources to clean up their balance sheets.

Given the higherlevels of impairment, SCBs (scheduled commercial banks) may remain risk aversein the near future as they clean up their balancesheets and their capital position may remaininsufficient to support higher credit growth.RBI's Financial Stability Report

The capital adequacy ratio of the banking sector as a whole remained largely unchanged in September 2016 at 13.3 percent.

Stress tests conducted by the RBI showed that under a ‘severe stress' scenario, while the system-level capital adequacy of banks would remain above the regulatory threshold of 9 percent, at the individual bank level, 23 banks, having a share of 40.7 percent of total bank assets, might fail to maintain the required level of capital adequacy.

They have considered a severe shock, but even if you look at a normal stress test, there are about seven or eight banks that will have the CET-1 ratio falling below the required threshold. Earlier this year we had estimated that the bailout cost for these banks would be around Rs 10,000 crore.Abhishek Bhattacharya, Associate Director, India Ratings & Research

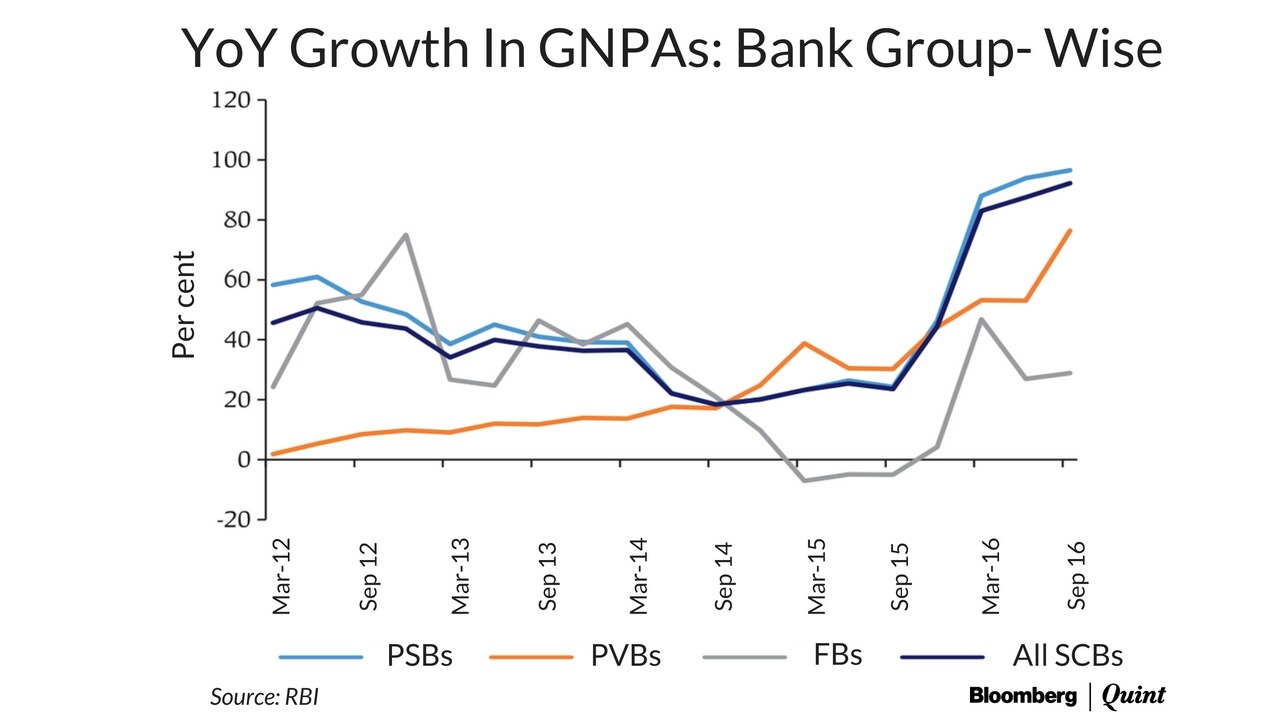

The reported asset quality of Indian banks started to deteriorate after the RBI initiated an asset quality review in 2015 and asked banks to classify stressed loans appropriately. This led to a surge in gross NPAs between September 2015 and March 2016. Since then the pace of increase in bad loans has slowed.

According to data compiled by BloombergQuint, bad loans of the banking sector as a whole increased by 6.6 percent sequentially in the quarter ended September, down from just under 9 percent in the June quarter. This is significantly lower than the addition of 33.9 percent seen in the quarter ended March 2015.

Still, the RBI in its report said that risks to the banking sector remained elevated and are higher than what they were at the time of the publication of the last Financial Stability Report in June.

Though the soundness of banks reflecting theircapital position improved further, continuousdeterioration in their asset quality, low profitabilityand liquidity contributed to the high level of overallrisk.RBI's Financial Stability Report

Credit Quality of Large Borrowers Declines Further

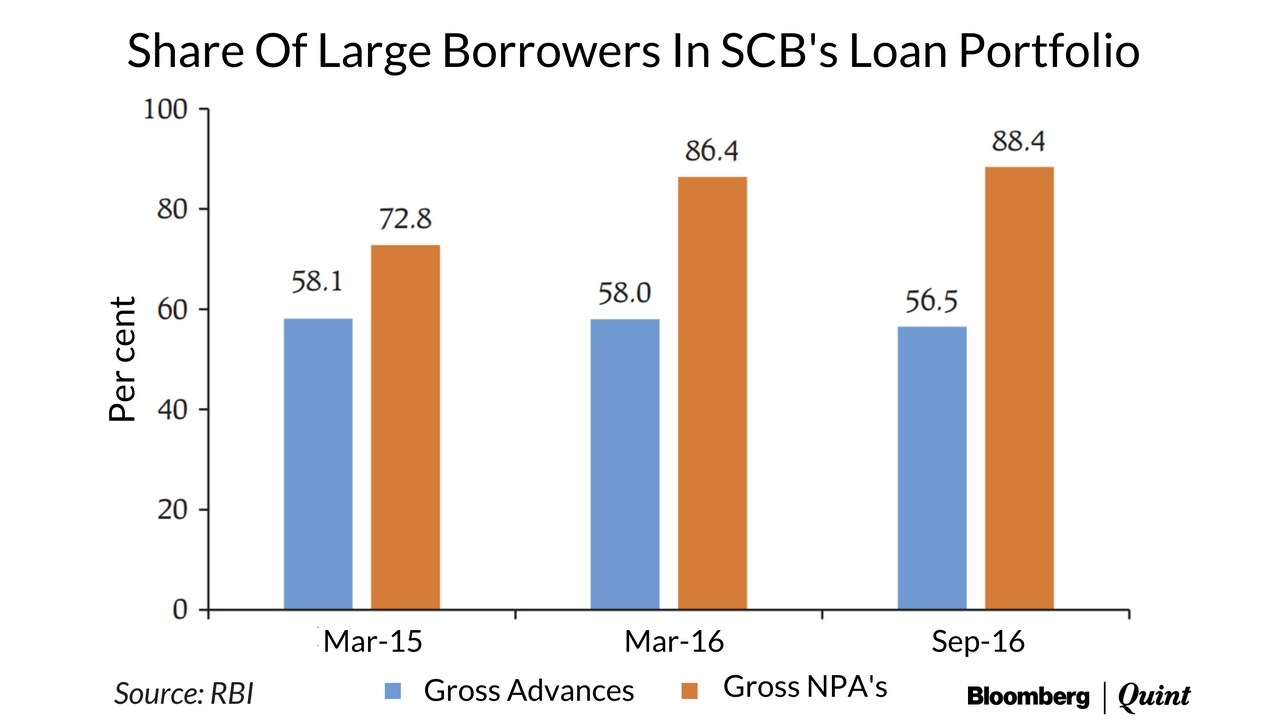

The total exposure of the banking sector to large borrowers, that is those with an aggregate fund-based and non-fund based credit exposure of Rs 5 crore, reduced, but asset quality worsened in the first six months of the year.

According to data provided by the RBI, the share of large borrowers in the total loan portfolio of the banking sector has reduced to 56.5 percent in September 2016 from 58.0 percent at the end of March 2016. However, at the same time, the share of these borrowers in gross NPAs has risen by two percentage points to 88.4 percent.

Current Provisioning Not Enough

The RBI believes that the current level of provisioning for bad loans by the banking sector is insufficient to meet expected losses (EL) as per the stress tests it conducted.

Currently public sector banks' provisions stand at 5.8 percent of total advances, while that of private sector banks is 2.3 percent. These provisions seem “insufficient” to meet the expected losses under stress scenarios.

Specifically, PSBs needto further increase their provisioning levels to meetthe ELs arising from credit risk, under baseline andadverse macroeconomic risk scenariosRBI Financial Stability Report

As per the RBI's report, 33 banks, which have a 74 percent share in the total advances for the sector, are unable to meet their “expected losses” with their current level of provisioning. The RBI has also noted that six banks, with a 7 percent share in total advances are estimated to have unexpected losses exceeding their total capital, based on stress tests.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.