(Bloomberg Opinion) -- Modern macroeconomics places great value on the idea of an independent central bank. Sitting above and apart from the political fray, wise central bankers are supposed to use interest rates so as to steer the economy between the Scylla of inflation and the Charybdis of recession.

President Donald Trump has little use for modern macroeconomics. In private remarks to donors, and again in an interview, the president lamented that his appointee, Federal Reserve Chairman Jerome Powell, had been too quick to raise interest rates as the U.S. economy revs up. As central bankers get ready for the annual Economic Policy Symposium at Jackson Hole, Wyoming, the threat to their tradition of autonomy must weigh heavily on their minds.

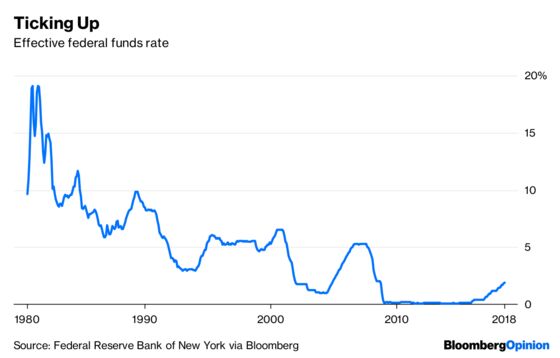

Why is Trump worried about interest rates? Although Powell has hiked rates five times, they’re still low by historical standards:

One reason Trump is upset is that he thinks low interest rates will help him win his trade war. This could be because Trump wants a weaker dollar. When rates are low, the standard theory goes, money tends to flow out of the U.S. to places that offer better rates of return. Those capital outflows require selling the U.S. currency, which pushes the dollar’s value down, making American exports cheaper and imports more expensive.

Another reason might be that Trump wants low interest rates to counter the economic damage from the trade war. U.S. manufacturers will be hurt by taxes on steel and other inputs, while American farmers will be hurt by retaliation from China and other countries angry at Trump’s aggressive policies. This could cause a slowdown or a recession that would be blamed — quite appropriately — on Trump. So naturally he wants low interest rates to give the economy a boost and help him weather the storm.

But there’s another reason Trump might want to jawbone the Fed into keeping rates low. Even scarier than the trade war is the business cycle itself. Rate hikes — even modest ones — could expose the weaknesses building up in the U.S. economy, and cut short the current economic expansion.

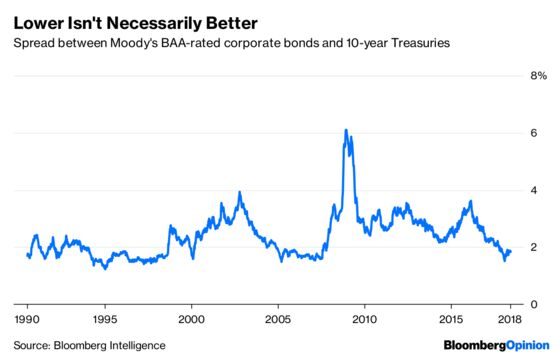

Historically speaking, it’s been a long time since the U.S. had a recession. According to some theories, long expansions tend to cause a buildup of bad debts in the system that eventually default and send the country back into recession. Research shows that when spreads between risky debt and Treasury bonds narrow, a slowdown often — though not always — follows within two years. As of this year, those spreads are looking fairly low:

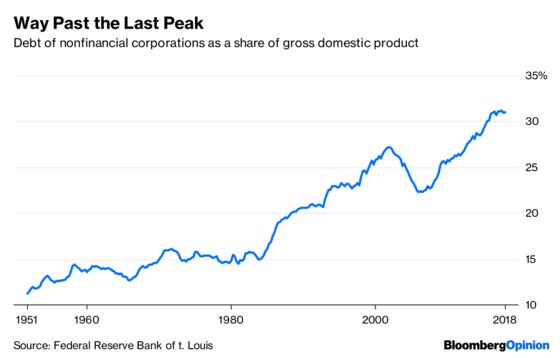

The question that naturally follows is: Where could bad debt be building up? During a recent debate with yours truly, Bloomberg Opinion’s Conor Sen suggested that the answer might be found on the balance sheets of American corporations. Though financial businesses are still less indebted than before the financial crisis, nonfinancial corporate debt is at record highs as a share of gross domestic product:

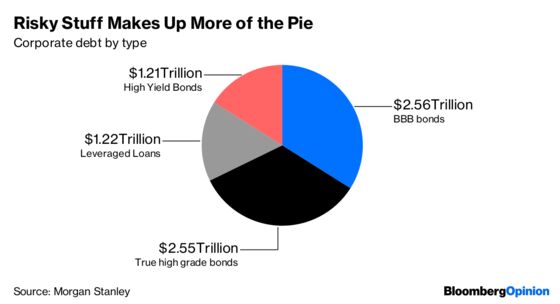

Jeff Spross of The Week has an excellent article that gives additional reason to worry. Not only is corporate debt increasing, but the share of risky debt in the system is rising. Research has also found that risky debt is a predictor of economic danger ahead. Although traditional junk debt issuance has fallen, other kinds of risky corporate lending are increasing. Leveraged loans — loans to companies that already have a lot of outstanding debt — are proliferating, more than making up for the decline in junk bonds:

Leverage magnifies risk — even a company that looks healthy and has a decent bond rating can quickly be forced into default by a small downturn if it has lots of leverage.

Additionally, medium-grade debt — bonds that are rated only slightly better than junk, and could easily turn into junk bonds if conditions worsen slightly — is ballooning, up more than 120 percent since 2011. And borrowing by truly safe companies has fallen. As Bloomberg Opinion’s Danielle DiMartino Booth has noted, this means the overall corporate-debt market is now looking very risky:

For now, profits are high, allowing corporations to support the high interest payments that their huge and growing debt pile requires them to fork over. But this precarious situation is unlikely to last forever. An economic downturn, or a rise in interest rates that made debt harder to service, could tip highly leveraged U.S. corporations into default. The large levels of debt would then amplify the severity of the recession.

Naturally, Trump would like to avoid such a scenario, which would send his approval ratings even lower and probably lead to Democratic electoral gains. The looming specter of a wave of corporate defaults might be one reason the president is growling at the Fed to keep the party going.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.