(Bloomberg Opinion) -- Splashing tens of billions of dollars on building the metaverse has gone down like a lead avatar with Meta Platforms Inc. shareholders, with its market capitalization down by about three-quarters from its peak of $1.1 trillion reached barely a year ago.

Chairman and Chief Executive Officer Mark Zuckerberg has gone rogue, but I find myself unsympathetic to shareholders' plight. Nobody forced them to purchase Meta stock and founder hubris is a risk you take when granting entrepreneurs nearly unfettered and indefinite control via super-voting shares. The dangers were clearly spelled out in Facebook's 2012 initial public offering prospectus and subsequent financial filings.

Though Zuckerberg's majority voting power is extreme such cosy arrangements became widespread during the free-money era, especially in tech, as startup investors and stock exchanges vied to appear founder-friendly or risk being shut out of the next big thing.

With luck, the rage and powerlessness Meta shareholders are experiencing will inspire capital providers and stock market guardians to impose sensible limits on dual-class voting.

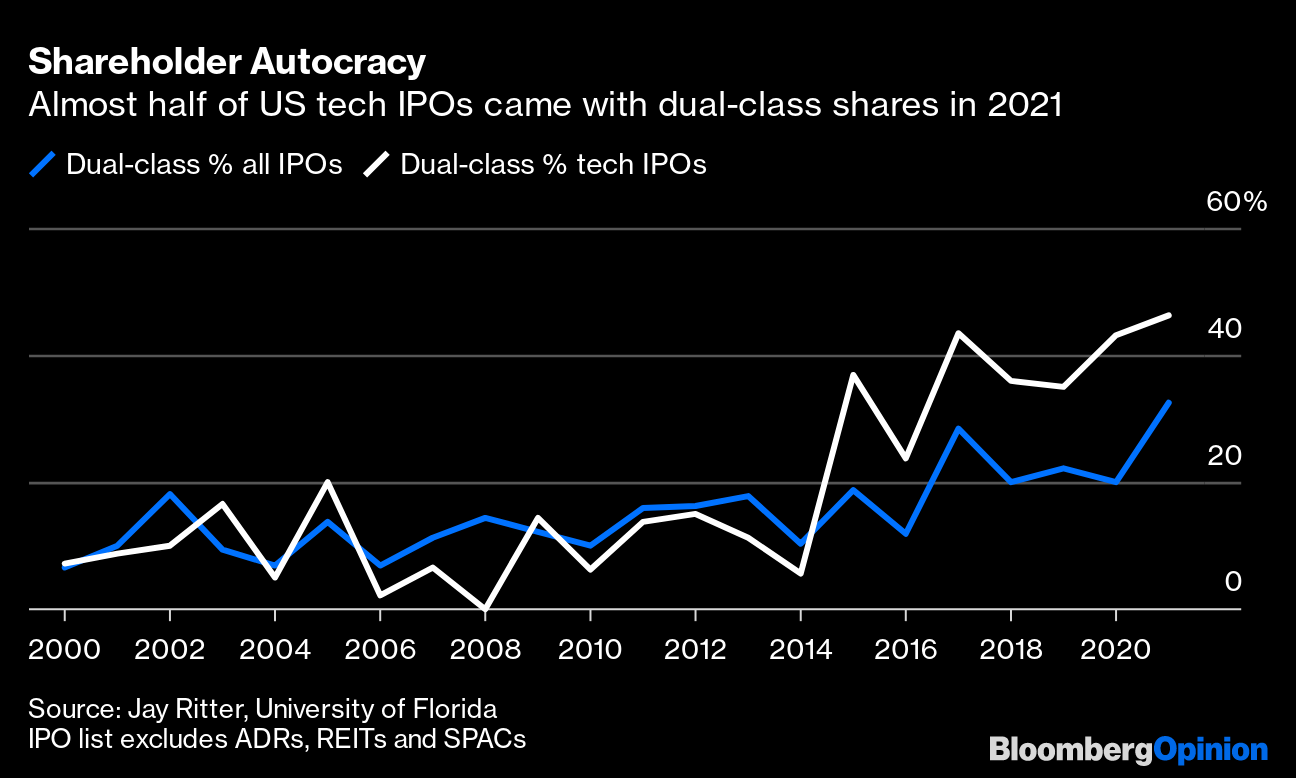

“One-share, one vote” enshrines corporate accountability, but the vital principle has become unfashionable in recent years. While family-owned businesses and media companies have long had dual-share structures, unequal voting rights really took off with the Google IPO in 2004.Last year, almost a third of the US's IPOs had dual-class shares, according to Jay Ritter at the University of Florida. The list includes Robinhood Markets Inc., whose ambition to democratize share trading didn't apply to its own stock. Like Zuckerberg, Robinhood's founders own a of the share capital but a of the voting rights.

The positive spin on stocks with extra voting rights is that they encourage founders to join public markets (rather than remaining private), while allowing them to plan for the long-term, not quarters. Thus they can be seen as a bulwark against risk-averse, dividend-hungry institutional investors or activists only interested in a quick profit.

Google shows this isn't totally wrong-headed: parent Alphabet Inc. has delivered outsized returns for shareholders while simultaneously investing in long-term moon-shot projects (some of which have flopped).

But I still think dual-class shares are the corporate equivalent of – conferring all the advantages of being a public company with few of the constraints. (Snap Inc. sold stock in 2017 without any voting rights at all!)Amazon.com Inc. founder Jeff Bezos coped just fine without such advantages while WeWork Inc.'s near implosion shows what can go wrong in the absence of guardrails.

Zuckerberg deserves respect for acquiring Instagram and WhatsApp when critics harped he was overpaying (he wasn't). But even brilliant founders can err or lack the skillset to deal with new challenges, such as online misinformation.

Shareholders need an insurance policy: How likely is it that all the businesses that went public with-dual class shares in 2021 are led by the next Larry Page or Sergey Brin? And when almost half of tech IPOs come with special stock, do investors really have a choice?

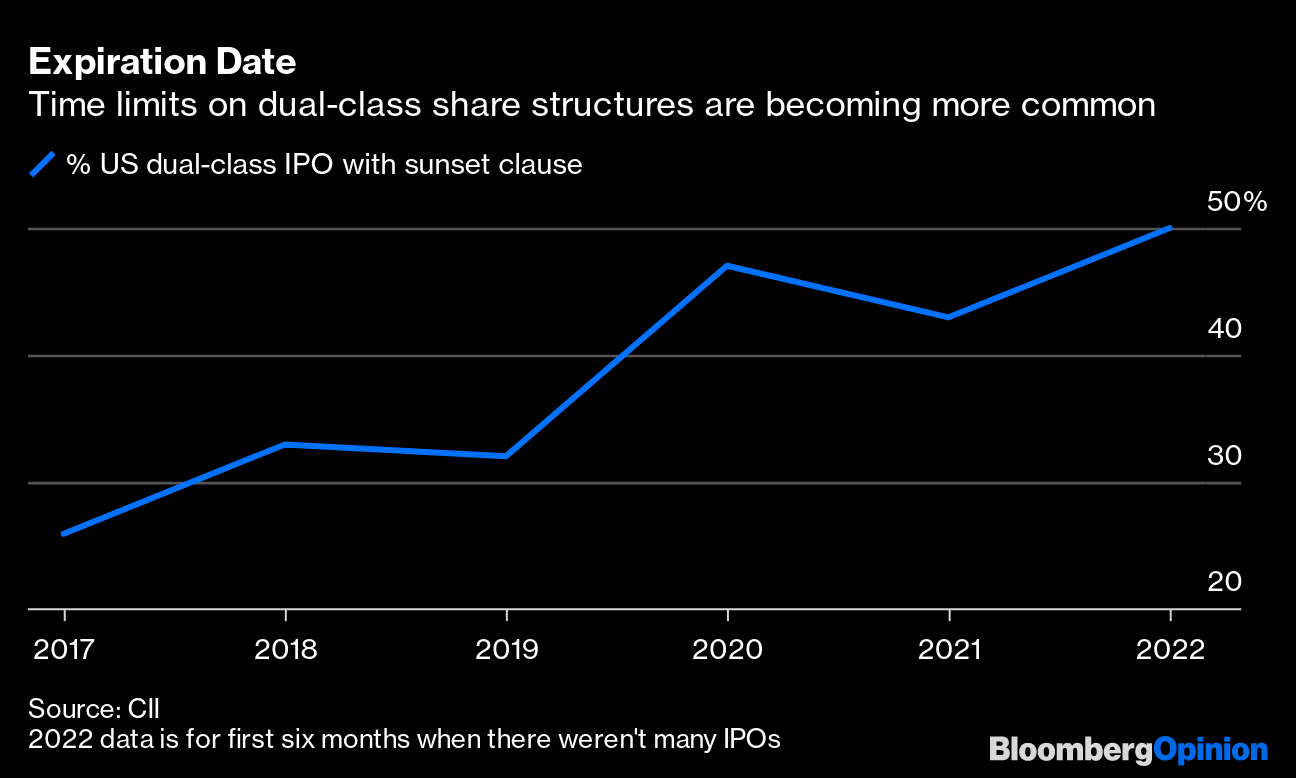

While dual-class shares can outperform, the effect tends to fade after a few years; at more mature companies investors often apply a discount to companies with unbalanced governance, such as Volkswagen AG. Unequal voting rights are encountering stronger resistance from stock exchanges, index providers, ESG-oriented investors and proxy advisors, leading to an increase in time-based sunset-clauses whereby super-voting rights expire after an agreed number of years (unless independent shareholders agree they should continue).

The Washington-based Council of Institutional Investors considers a maximum seven-year duration good practice, while recent UK reforms settled on a five-year limit – offering a balance between protecting the firm while it is young and making it more accountable once it has grown up. (The median age of companies that listed in the US last year was 11 years; many aren't therefore neophytes in need of patient nurturing).

Regrettably several companies with sunset clauses have adopted much longer protections: Founded in 2008, Airbnb Inc. opted for a 20-year sunset clause when it went public in 2020.

This nascent revival of shareholder democracy and governance norms looks sustainable: Investors should be more wary about sinking cash into overvalued startups. Founders wanting to raise capital (whether in public or private markets) will have to offer co-owners more concessions.

Had the seven-year recommendation been applied at Facebook, Zuckerberg would have lost his super-voting rights in 2019. But as Meta doesn't need to raise more money, shareholders must rely on him seeing the error of his free-spending ways. They can't say they weren't warned.

More From Bloomberg Opinion:

Zuckerberg Should Focus on the Midterms, Not the Metaverse: Parmy Olson

The Problem With Dominant Mark Zuckerberg Types: Chris Hughes

Zuckerberg's $1,499 Headsets Won't Help Meta: Parmy Olson

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies in Europe. Previously, he was a reporter for the Financial Times.

More stories like this are available on bloomberg.com/opinion

©2022 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.