(Bloomberg Opinion) -- Despite the euro zone having lower official interest rates and a notably softer economy than the US, the euro has held up remarkably well against the dollar. The foreign exchange market's most popular currency pair trades not just in line its $1.085 average of the past year but within reach of the $1.11 five-year mean. The common currency, however, can't defy gravity forever — so a return toward parity with the greenback looks more likely than not over the course of this year.

At about 6.6%, the exchange rate's volatility is the lowest it's been since November 2021, having fallen from nearly 11% a year ago and illustrating how becalmed the market has become. This peaceful state may prove transient; given that rate-cutting cycles and recessions tend to hit the weaker side hardest, the euro looks increasingly vulnerable.

The two main drivers of currency values are relative central bank interest rates and respective growth outlooks Both are fading faster in Europe than stateside. It's not just about absolute measures, but how those respective differences contract or widen that typically influence the foreign exchange market. On both measures, the US position looks superior, with the dollar also underpinned by its status as the world's reserve currency.

One other salient factor is investor positioning. Bank of New York Mellon Corp.'s proprietary iFlow system tracks its global custody client holdings which, worth $46 trillion, are the world's biggest. On balance, clients remain overweight in euros. Geoffrey Yu, the bank's senior strategist expects euro-dollar parity to return, not just due to fundamental economic and monetary reasons but because investors are shifting rapidly from being extremely long of euros.

An exodus out of the common currency amid the energy-price shock following Russia's invasion of Ukraine saw it fall below parity with the dollar for most of the final months of 2022. Asset owners had shifted steadily back into euros over the last 18 months but their enthusiasm is waning. Yu reckons holding euros has been used by investors as a counterbalance against too much exposure to better-performing US markets. But risk-on assets such as US tech stocks are increasingly seen as one-way surefire bets, while for risk-off safety a 5.4% yield on US Treasury bills is hard to beat. Being overweight euros may no longer be the optimal choice.

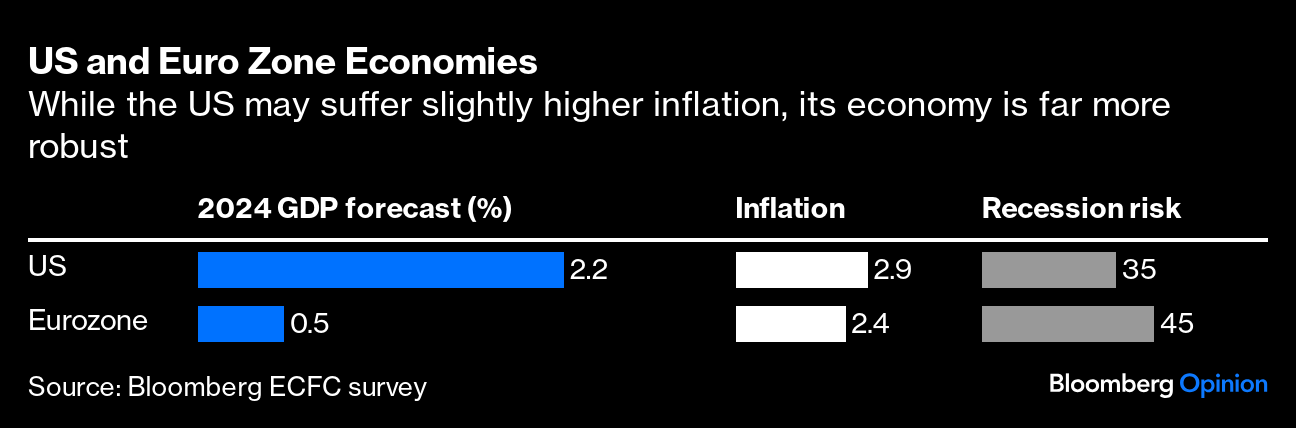

The relative economic outlooks for the two largest global trading blocs are markedly different, not just over the recent past but also with regard to future expectations. It's somewhat puzzling how strong the euro has been, but it's partly explained by the 2.5% increase in its trade-weighted value in the past year, aided by the relative currency weakness of some its big export markets like China and Russia.

Inflation has been in steady decline globally. Both US and euro-zone consumer price measures peaked at just over 9% in mid- to late-2022, with February seeing euro-zone inflation dropping to 2.6%, lower than the 3.1% figure for the US. But on the growth outlook, there's no competition. Deutsche Bank AG's monthly client survey has shown a steady shifting away from concern last year about an impending US recession to a large majority now expecting either a soft landing with growth remaining positive — or no landing at all. Fourth-quarter US gross domestic product rose at an annualized 3.2% pace; the euro zone economy stagnated.

Moreover, the euro-zone's future remains bleak. Most worrying is that the bloc's biggest economy, Germany, is struggling with a collapse in exports and an end to its cheap Russian energy. It's likely fallen back into recession at the start of this year from which it doesn't look like suddenly bouncing out of. The rest of the bloc is either in or close to a recession, with a lackluster scenario for the next few years at least; economist are forecasting growth of just 0.5% this year, compared with 2.2% for the US.

On interest rates, the European Central Bank is making loud noises about cutting its deposit rate in June. President Christine Lagarde has valiantly tried to restrain expectations for what will come afterward, but the market isn't really in listening mode — once the first reduction is in, a cascade of cuts is typically anticipated. The Federal Reserve is still making warm sounds about looser monetary policy this year but it truly is data dependent. The US economy is still sufficiently vigorous to keep inflation concerns alive. Both central banks may well cut rates in June; but while the futures market puts the odds of a Fed move at 63%, the ECB's likelihood is at 84%.

A weaker common currency appears to be the course of least resistance for the foreign exchange market. The ECB governing council may well be content to watch it gently weaken, as it would boost its export-led economy. It'll want to avoid any sudden lurches lower — but benign neglect toward the euro may form part of the central bank's strategy in the coming months.

More from this writer at Bloomberg Opinion:

-

Gold Setting Records Is Exuberantly Rational: Marcus Ashworth

-

Rate-Cut Bets See June as the Kindest Month: Marcus Ashworth

-

Sterling Assets Offer Lucrative Places to Hide: Marcus Ashworth

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. Previously, he was chief markets strategist for Haitong Securities in London.

More stories like this are available on bloomberg.com/opinion

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.